Dear investors and well-wishers,

The fund declined 6% in August, but after a strong September, we’re now up ~45% net for the calendar year-to-date.

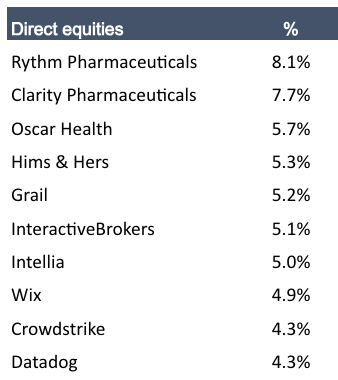

We’ve been highly focused on healthcare this year. Of our top 10 direct equity positions, 6 are healthcare-related, including all of our top 5.

This is partly because some of our fast-growing semiconductor stocks like Credo and Astera hit their profit targets after only a few months, and of course our holdings below may evolve significantly.

Some of our recent purchases have moved almost immediately - Intellia is up 44% on our average buy price, and Grail is up over 50% from our average price, which is quite an achievement from our quant models, as both these companies have been fairly disastrous for long term holders. Intellia is still down 90% from its 2021 peak.

Top 10 snapshot

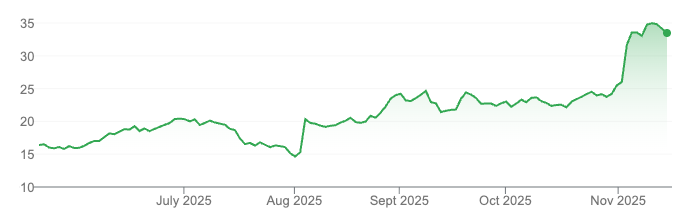

Grail

Grail is a new position, though I’ve followed the company for the better part of a decade.

Grail’s stock price

The name is apt: Grail is pursuing a holy grail of oncology: a simple blood test that can detect cancers before symptoms appear, a goal that has eluded researchers for decades.

Their test, Galleri, analyzes methylation patterns in cell-free DNA using machine learning to identify a cancer signal and its tissue of origin.

The science is plausible: it’s been known for decades that tumors shed fragments of DNA into the bloodstream. The challenge was whether these could be reliably decoded, and translated into improved patient outcomes. The test has been in the market for some time, but until recently struggled to get traction.

The Challenge

Doctors have pushed back for good reason. For those of us outside the profession, it seems obviously helpful to know if you have cancer. But treatments often come with life-changing side effects. Even the next set of tests, which often include invasive biopsies, carry serious risks.

The issue is compounded by the maths of general population testing. The economics are hard to prove, and given most tests are negative, the number of patients required to prove a particular thesis is large. Building out survival data is a lengthy, expensive proposition.

To win over the medical community, a new test needs to go further than proving it can detect cancer, it has to show that this early detection extends life. Various promotional press over the years probably hasn’t helped win over sceptical physicians.

Grail has lived up to its name in other way - it has consumed vast sums of capital for little reward.

Illumina purchased the company for US$8 billion in 2021, and by then the company had already raised $3 billion. The company was divested, and has continued to accumulate capital losses on the Nasdaq, most recently almost $500 million over the last year.

For all the money spent, the company is now worth about $2 billion.

Other companies working on cancer diagnostics generally target a specific indication, where it’s easier to build stakeholder support and do the large studies required to demonstrate long term improvement in survivability and outcomes, and economic savings for end payers.

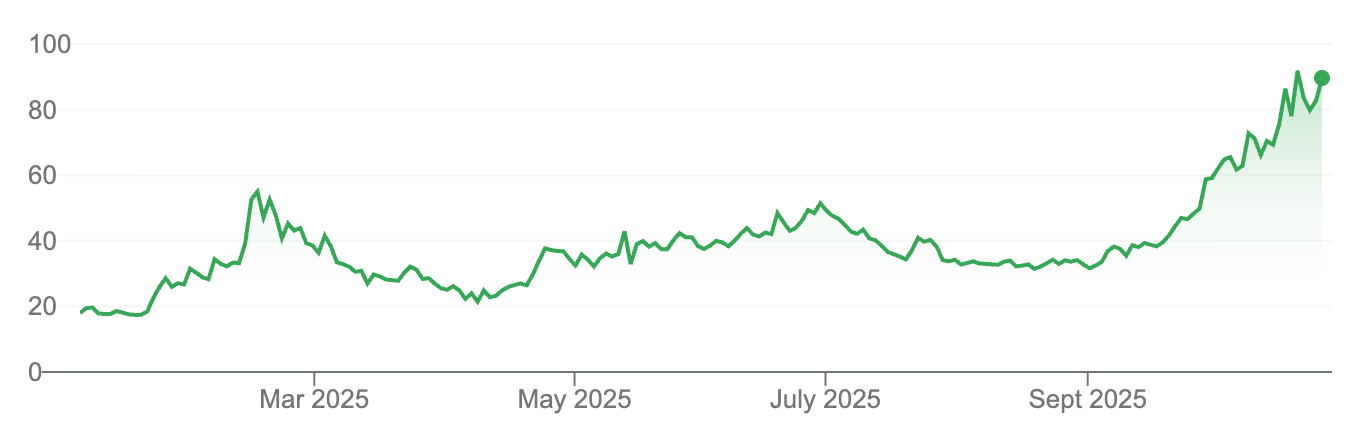

A notable example is Guardant Health’s test in colon cancer, which is gaining traction:

Guardant Health

Grail is uniquely advanced in targeting the more ambitious goal of a multi-indication test.

In June this year, Grail announced positive results from their registrational 35,000 patient study PATHFINDER 2, initiated in 2021 to evaluate multi-cancer early detection in their target market of asymptomatic adults over 50.

Grail reported a positive predictive value (PPV), or likelihood that a positive Galleri test was confirmed to be cancer, of 43%, specificity of 99.5% and 88% accuracy in determining tissue of origin (link).

Pathfinder 1 showed that Galleri could double the amount of cancers found in general screening, and the latest data suggest their updated test is performing better. More detail on the complete 35,000 patient study will be released mid 2026. As mentioned, these trials are long, large, and expensive!

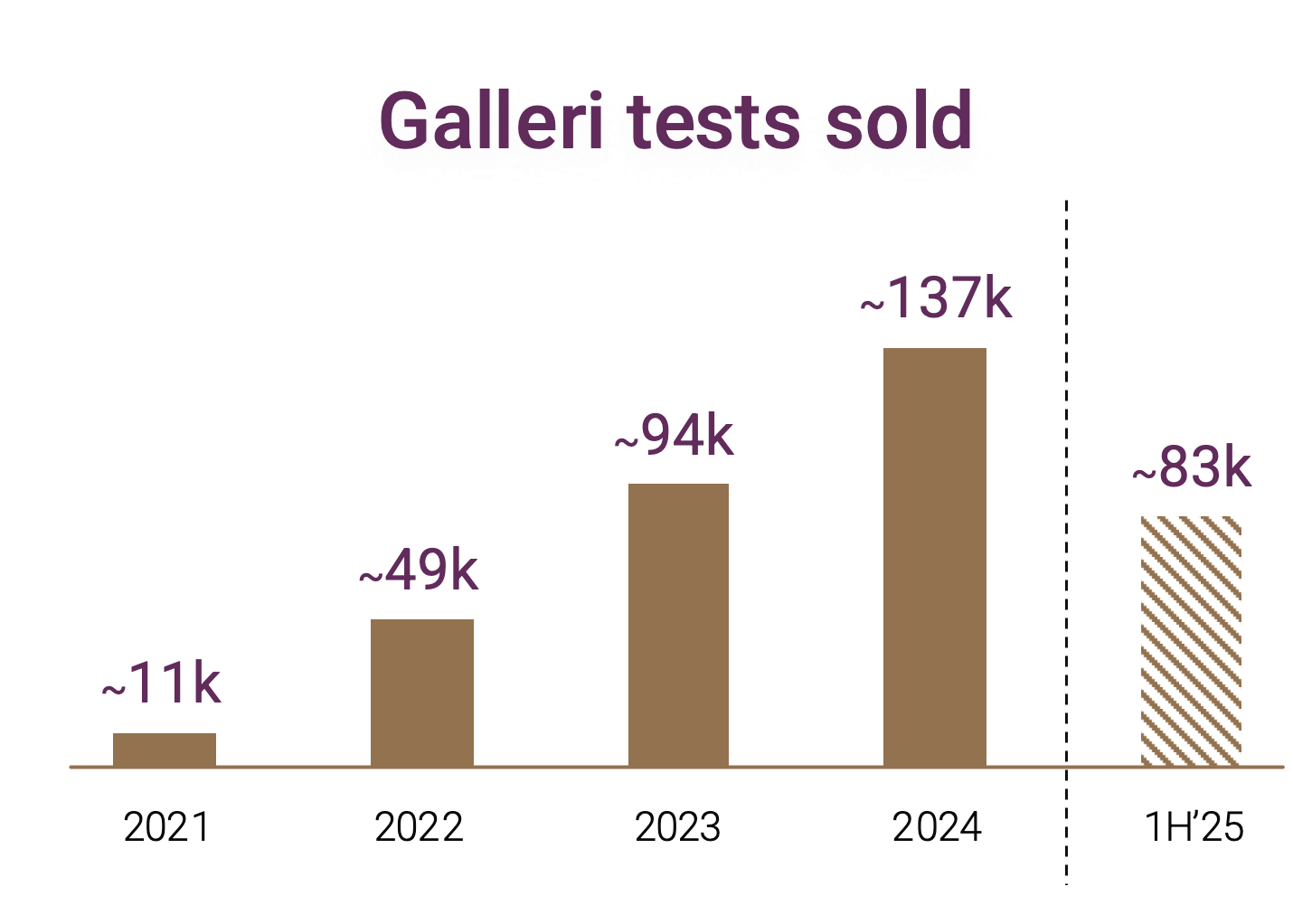

In real world settings the test is also performing. In April this year the company released data on 100,000 patients that had purchased the test, reinforcing prior positive results on sensitivity and cancer signal origin accuracy.

Galleria is not FDA-approved, but can be sold with a prescription. The test is gaining traction:

The company is preparing an FDA submission for Galleri as a medical device / diagnostic product in the first half of next year, which is the key catalyst that would significantly increased adoption and bring forward reimbursement.

I’ve always found the company intriguing.

The cash burn is significant, but the prize is substantial, with an estimated market of over $100 billion. Many billions have already been spent, and this is only a $2 billion company.

But as with gene therapy, it’s no longer 2021, and these companies have made significant progress over the last few years.

With FDA approval possible in the near term, test volumes increasing rapidly, a growing body of supportive evidence, and a market cap of $2 billion, there is clearly a >10x opportunity here if the company executes.

For a company with such high risk/reward risk management is critical, and our systems gave us a buy signal only a few weeks ago.

There is significant path dependence here. The cash burn is immense, FDA approval and timelines are uncertain, and even in the best case there’s a lengthy time to cash flow breakeven. The company could advance several fold and collapse multiple times before it’s generating significant profits.

Our quantitative approach should allow us to harvest profits if the company performs, and avoid the worst case if timelines stretch out and dilution blows up the stock price.

A long term buyer today could be right on the ultimate success of the approach, but suffer a similar outcome to Illumina - something we’re going to be careful to avoid.

Sometimes when researching one company, a new idea pops up.

In February this year Grail announced a partnership with Quest Diagnostics to make their test easily available through Quest’s platform. Quest has also done a deal with Guardant Health, which after a similarly long and painful cash-burning period is on the cusp of significant increase in revenues.

Guardant revenue (US$)

As these tests mature, pass FDA and reimbursement guidelines, and hopefully are widely prescribed and improve cancer detection rates, Quest may also prove a strong performer. And as a larger profitable company growing EPS at over 20%, the risk is much lower, and there’s multiple ways to win.

Outlook

The market has been rallying for five months now, so naturally everyone (myself included) has started to wonder when the next inevitable sell-off happens.

So far it seems every time the market wobbles new AI deal is announced and settles things.

The handful of decision-makers running US trillion dollar tech companies are still firing ahead with capex. And as we move into mid/late cycle in semis, the rally has broadened out, with more struggling companies starting to perform.

Oracle was the latest in the headlines with a deal announcement with OpenAI, and Intel looks like it might finally join the winners club.

It’s certainly a high priority for the United States for Intel to succeed as they try and reverse decades of manufacturing loss to China and in the case of semiconductors, Taiwan.

Intel - joining the AI winners club?

It’s been fascinating to watch Google compete and make major changes to their largest product, search. There have been multiple times in the ChatGPT era when their core business was challenged, with the first major losses in search market share that I can remember.

But they integrated AI into search results, rolled it out to billions of people, started the feedback loop, and are now offering a ‘dive deeper’ button that takes searchers straight to their dedicated AI platform.

And of course as AI moves multi-model the immense content uploaded daily to YouTube will ensure plenty of fresh live training data.

Their prescient bet on designing their own chips has also paid off: they are the only GPU-using company not entirely beholden to Nvidia.

Larry Page has repeated internally that he’s willing to go bankrupt to win in AI, but it doesn’t look like Google will need to.

Google stock price

While we’ve been almost as bullish anyone on semiconductors, our recent successes have actually been in US healthcare.

Australia has still been a significant detractor for us this year, though Amplia, Syntara and Clarity have had strong years from a clinical perspective, and Curvebeam AI just completed a raise.

Even after this rally, we are still finding opportunities, with new entries into companies like Grail and Intellia, and even software with Crowdstrike and Datadog. And having a risk management process means we have clearly structured exit plans if the rally continues or reverses.

Best

Michael