Dear investors and well-wishers,

We finished October up 0.7%, which took us to 39% pa over the last three years and the #1 fund in our Morningstar category.

Over the last two years we’ve returned 74% per annum, which is an important milestone as it’s now two years ago since we revamped our strategy and implemented a quant approach across our growth portfolio. Our seven year number is 11% net, though I suspect we would have done substantially better if we had developed our approach to risk sooner.

Regardless, our entire focus is on the next two years.

Over the last 6-8 weeks these models have given sell signals across neoclouds (Coreweave, Iris, etc), quantum, nuclear, drones, and all kinds of small caps, and we sold a number of positions which have subsequently deteriorated.

After a stonking retail rally, where (for example) some quantum stocks advanced >30x in a year, we were due for some kind of unwind.

Neocloud sell-off

Suitably for the times, the two key moments that rattled the sector happened on podcasts (and two of my favourites, no less).

The first was when Sam Altman, CEO and cofounder of OpenAI, was asked the very reasonable question of how he planned to fund a trillion dollars of capex on tens of billions of revenue.

A not unreasonable question, and one you’d assume an answer had been well-prepared. Instead, he became defensive, and aggressively offered to find a buyer for the interviewer’s shares if he was so unhappy.

By all accounts Sam Altman is a slick operator, but he seemed to forget himself and revealed either an inner conflict or perhaps a blind spot, on an issue which is existential for his company.

Separately, in a pod with Dwarkesh, Microsoft CEO Satya Nadella made his own views on neoclouds clear, characterising the businesses as ‘bare-metal services’ and being more than happy to take the high margin part of the stack.

There are a large number of bitcoin miners who, on the brink of bankruptcy, found themselves with the perfect sites and perfect infrastructure for the biggest datacenter buildout in history. I’m sure they can barely believe their luck.

But as with bitcoin mining, they are commodity suppliers, only worse, as this time they have a higher cost of capital, less expertise, and lower access to GPUs than the hyperscalers they proudly report as customers.

Satya Nadella spelled out what we had already noticed from his actions - he’s happy to offload this risk on to someone else. Which is particularly important as the key risk to neoclouds here is that Microsoft stops being a buyer, and he’s the CEO!

Which is no shade on commodity suppliers.

As with equipment leasers to massive mining companies - who can also afford their own equipment but sometimes choose to rent - they can scale up fast and generate outsize returns in shortages. But even a minor oversupply (which the massive sums of capital in neoclouds now all but guarantee) can lead to disastrous pricing dynamics.

The market gods have provided these fast-pivoting bitcoin miners with a gift, and {in my opinion} it behooves the management teams, and certainly investors, to convert that luck into cold hard cash as fast as possible. Which is exactly we’re seeing over the last few weeks, and the publicised efforts for those still private to list as soon as possible.

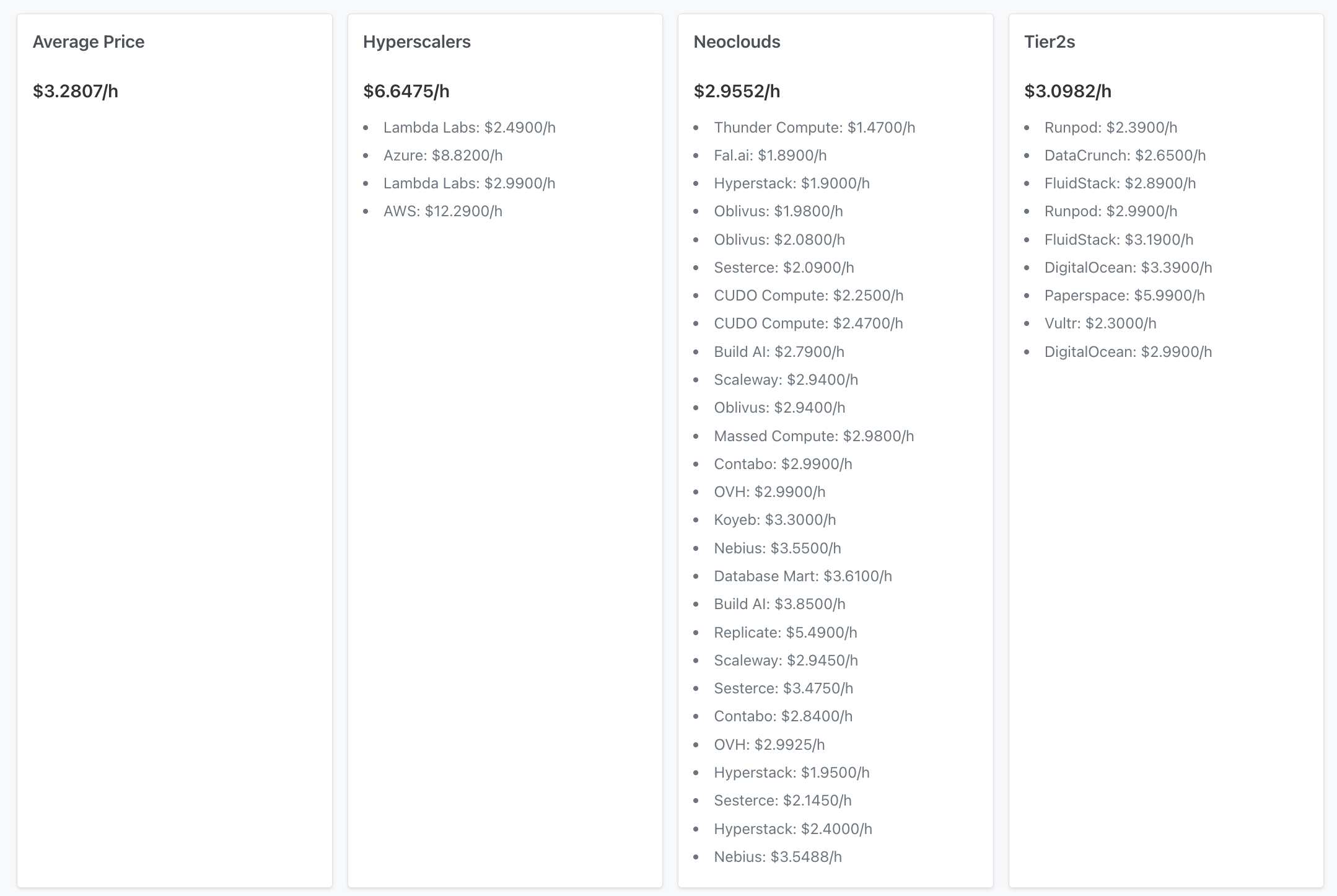

Coreweave is now down 45% over the last month, and 59% from the highs.

The financials are ugly: in the midst of a boom, their net interest margin is -$100 million, but this excludes their main cash expense, which are the prodigious sums of capex running through their balance sheet.

This is what I mean by commodity suppliers:

The Aussie companies don’t even make the list!

Healthcare

One sector our models have kept us firmly invested in is US healthcare, with new companies like Castle Biosciences performing well:

Frustratingly Day One made an acquisition. We’d prefer our companies being bought, not doing the buying, but what can you do.

We’ve had a number of conversations with offshore investors and allocators recently, and I was surprised how quickly every discussion turned to healthcare. Usually it’s semiconductors, big tech, and more popular parts of the market.

There are ~40 US healthcare companies with market capitalizations of over $1 billion growing at over 40%, so this is an exciting part of the market for our kind of strategy, and so far healthcare is moving independently to the chaos elsewhere.

Confusingly, the US administration seems to be pulling in two different directions. uniQure announced positive results in a trial for Huntington’s, and the stock pentupled as in discussions during the trial design period the FDA guided they would allow early access.

But a week ago the FDA kibboshed that idea and wants another trial with placebo/sham control. Which would have been a lot easier to say three years ago.

QURE’s gene therapy requires brain surgery, so on the one hand, we can all agree there is insufficient data to say definitively their treatment works.

But on the other, asking suffering patients to undergo surgery without getting the drug, and many others - with a degenerative disease no less - to wait several years for an outcome, seems unbalanced, and contrary to the administration’s statements around speeding up approvals.

It’s all well and good to want more data, that goes without saying. But taking a hard line means many working treatments will never reach the market. Biotech is already barely economic, and on average, even a loss-making proposition. It’s hard enough at the best of times to justify investment into unquantifiable biological risks along with the usual set of problems companies periodically have to face.

In my (uninformed) opinion it would be far better to allow dying patients more freedom to try new treatments, particularly if they can pay for them, and then make the best possible use of the additional data.

This is the number one debate in healthcare. How will the new FDA balance scientific rigour with the important goal of reducing costs and developing new drugs?

Have regulators set the bar too high, slowing drug development and blocking many lifesaving drugs from ever reaching the market at all?

From my seat it seems so. Too many promising treatments don’t get funded. The timelines are too long, and the capital needs too high. Every month that it takes to review a submission adds significantly to the cost and eats away at the value.

A local example was Syntara, which was asked to do a second Phase 2 trial before a pivotal trial. Again, we can all agree extra data is helpful. But that pushes the entire timeline out years and adds serious cost, not to mention taking years off the patent life and the end value that is supposed to justify all the investment and waiting around.

From Australia, all we can really do is watch and hope they get the balance right.

Huntington’s patients are certainly going to fight for this one.

Path forward

We’ve been net sellers for the better part of two months now.

The same algorithms that worked so well for us over the last two years can also work in reverse, in down markets, though we almost always be long-biased.

Shorting is frustrating because it’s easy to find companies that will almost certainly go down, but still exceptionally difficult to make money.

The same stocks worth next to nothing have a nasty habit of going up 30,00% every now and then, not least because everyone knows they’re going down, so gets caught short together.

If I had to guess (note, this is market musing, we will follow our strategy regardless) this is how I think the market plays out:

- Quantum, neoclouds, and nuclear retail favourites continue to sell-off.

- This spreads to major market indices,

- The algos that drove the bull and bear markets this regime will be triggered again, leading to hundreds of billions of dollars of forced selling.

- Delinquencies and bankruptcies have already started trending up in Australia and the United States, and this spooks central bankers, which start to cut rates.

There has already been significant weakness in discretionary retail names, restaurants and the like.

Australia is in a thorny position as Government spending has swamped the private sector. In some age groups more than 1/6 young people are on disability benefits, and most hiring has been Government-related, which adds an inflationary pulse and less room for bankers to move. Markets could collapse and those on high-paying Government jobs will still be bidding on real estate.

Housing subsidies are adding fuel to the fire, and these should really be better accounted for in inflation statistics, given they’re most of our largest expense.

But these are just guesses, and not necessarily related to markets.

As Druckenmiller once notably pointed out, soft economies can be excellent environments for stocks, as the only tools available are to cut interest rates and add liquidity, and that invariably finds its way into the pointy end of risk markets (which includes growth stocks).

We’ve now cut exposure substantially, and while there is still some way to go, our quant models have started taking us out of a number of our favourite stocks. That’s actually the most comfortable place to be, as we can sit out turbulence and wait for the next set of buy signals, whether they come tomorrow or in some time.

Nvidia is about to report, so that could settle the market. Some of the most profitable companies in history are taking on substantial debt with the sole purpose of buying, installing and operating banks of Nvidia GPUs.

It’s not trading expensively relative to current earnings, but analysts will pour over its guidance, and back out how much spend is going towards neoclouds and companies where Nvidia is not just the seller, but also a key investor and end purchasor of leased capacity.

Long term, I’m as optimistic on AI as most, and our strategy is designed to capture the bulk of this trend which might continue throughout our lives. But perhaps not right now.

Michael