Dear investors and well-wishers,

Our fund rose 13.4% in September, which lifted our 3 year IRR to 36% net and put us at #1 in our Morningstar category. So we’ve made some progress over the past few years. Our goal is now to extend this and post a strong five year number in two years time.

A turn in US biotech

We had some wins - and booked some early profits - catching a turn in US biotech, which has been in a four year bear market.

There are around 40 companies with a market cap of US$1 billion+ growing at over 40%. The sector has turned, and positive news is leading to rapid gains off very low bases. The market is behaving here, and quality is getting paid.

I’m focusing most of our work here, and over 50% of the fund is now invested in healthcare, divided between early stage biotech in Australia and fast-growing revenue-generating companies in the United States, where there’s enough liquidity to use our quant models to manage risk.

Avadel had a take out offer:

We took some profits in Grail:

But it hasn’t all been smooth sailing.

A patient was hospitalized in one of Intellia’s main programs, knocking the share price back to ~$15. We bought at ~$12 and sold 40% systematically on the way up, so we’re moving to the sidelines on this one now.

Market set up

The debate around semiconductors heated up, with AI folk hero Andrej Karpathy casting doubt on some of the more promotional AI predictions. If you have a few hours to spare, his educational material on LLMs is the best.

The hyperscaler use of third party datacenters is a clear indication where they expect the residual value of the current crop of GPUs to land. Megatech cos have the expertise and capital to build out their own supply, so choosing to lease is a telling strategic choice.

There’s also new willingness to use debt to fund capex, which if continued, will change the balance sheet dynamics of these companies. Oracle was the latest with a $38 billion debt deal after Meta’s $27 billion deal. Depreciation and the rate of obsolescence of GPUs is far from clear, and the profitability of this debt capex will depend on where these numbers land.

In the prior regime these companies generated (and mostly sat on) mountains of cash.

But it doesn’t pay to get too bearish too early. As of today, datacenter capex is steaming ahead and is meaningfully increasing GDP growth.

There is also a marked upturn in LLM usage, so end user demand is healthy, even while major LLMs are operating at a loss.

I’ve written before how big tech companies are modern toll roads, inserting themselves as a cost item for every person and business. Apple bills almost every wealthy consumer, Microsoft bills every office worker (if they raise the price of Office, what are you going to do, lose access to Word and Excel?) and Google and Meta tax every business that wants to advertise.

In different ways these are the ultimate global business models, and with rare exceptions it’s impossible to succeed in the West without paying more and more, whether in advertising, office seats, or compute capacity. And as industries changed and different companies won or lost over the past decade, the winners always ended up with larger bills.

Now, Nvidia has slipped to the top of the food chain and is tolling the toll roads, inserting themselves as a cost item above the hyperscalers, billing them so much they have to go into debt to fund 75% margin GPUs.

It’s another win for passive investing.

Active managers had to spot that shift two years ago and bet big on it. Passive investors won anyway, as Nvidia rose through the index.

This is an unappreciated benefit of passive: when there’s disruption the winner usually rises through the index. And when disruption does happen, it’s usually a tiny number of companies disrupting many more, so active managers tend to lose.

Losers become cheap before they go out of business, so invariably discretionary managers think they see a value opportunity, precisely when the disrupter is becoming a larger part of the index, and the disrupted a smaller. Think of all the retail companies that became value favourites as they shrank, before being finally crushed (along with their concentrated investors) by Amazon.

There’s another feature - in living memory this has mostly applied to the United States, as US tech companies haven’t just disrupted US industries, but global industries, capturing value from indices everywhere else in the world. And the AI boom came from the same Californian suburbs as so many prior tech revolutions.

If there’s a hiccup in the coming earnings season, it will likely be because capex figures come under question, or perhaps the hyperscalers pull back on the second derivative, the growth-of-the-growth of their spend. At some point in this cycle they will guide to flat year-over-year capex, which will be tough for the market to swallow. But so far we are not there.

The market zoo

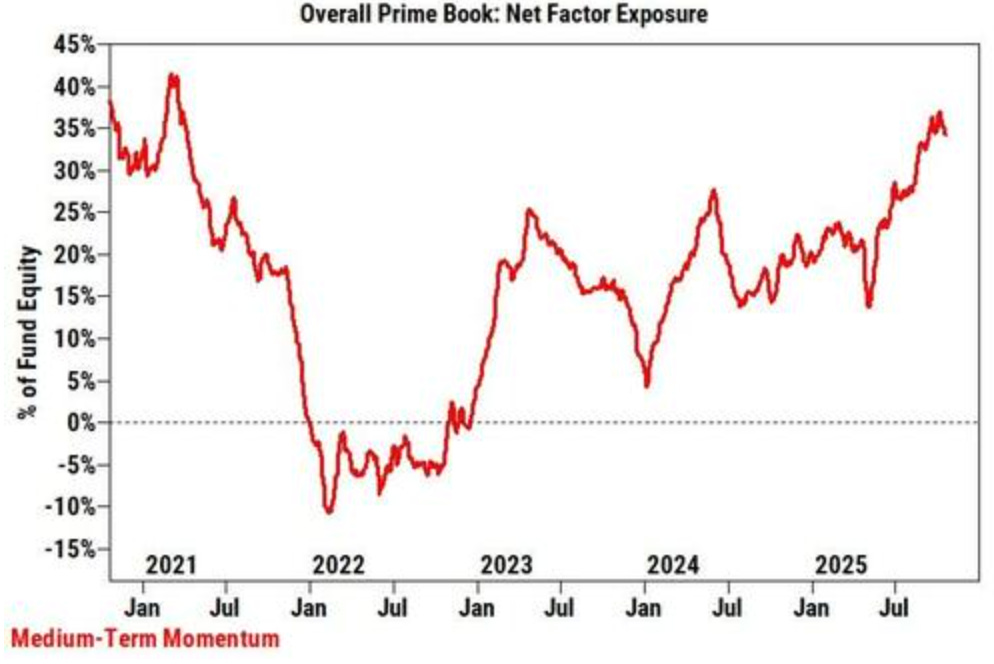

Tracking the different market animals has been very helpful this cycle. Quite a lot has changed over the last few months, so it’s worth checking in how everyone is positioned.

- Momentum/CTAs/vol targeters

There’s $250 billion to perhaps a trillion+ in momentum strategies, including trend-following CTAs and volatility targeters like Bridgewater. There has been a lot of chop and volatility over the last couple of weeks, which means there will be some level of automated selling.

Whether this spark in volatility is enough to light a market bushfire is impossible to know in advance, but these strategies are close to max invested, so the next big quant move will have to be to the downside.

This is the most uncomfortable part of the market today.

- Retail

Retail is more powerful than ever, and retail buying over the last 30 days was the highest on record, more so than in 2020 and 2021.

Even without the data, you can see this in the significant outperformance of retail favourites this year, often against heavy institutional short-selling.

The most speculative end of the market looks particularly exposed, like innovation areas of quantum computing, where significant breakthroughs in mathematics, physics, and material science are still required for these companies to achieve anything. These companies are a long way from commercialization, and they’re chasing a moving target in GPUs.

Retail sentiment and momentum will drive these stocks for some years to come, as there is no revenue or profit pull to attract the other market animals.

They’ve been great momentum stocks on the upside, and will likely prove so on the downside. That’s the best way to play these, if you must, as sober analysis would certainly have led to losses rather than profits so far this year.

A viral tweet or reddit post can summon tens of thousands of retail buyers at the open the next day, so fighting this makes little sense to me. It’s just the way markets are right now. These surges unwind, but only when flows reverse. Momentum can catch both moves.

But there’s always the popcorn option: watching the swings, debates, profits and losses from the sidelines. Which certainly beats being forced to buy back stock in a company you know is going down, but has just gone up ten times.

Other parts of the market are better behaved right now.

- Institutions

This has been a long suffering part of the market. Many active managers missed Nvidia, which posted the largest $ increase in value over the past few years so has been particularly painful.

Institutional favourites are also plagued by outflows towards passive, and as institutions either have avoided or shorted the high performing retail favourites, the underperformance this year has been particularly tough (to the benefit of retail and quants).

And earlier this year the sharp swings tripped up slow moving institutions, many of whom publicly called for a global tariff-induced recession. For whatever reason, that hasn’t happened, though I personally would have guessed so, along with so many others (thankfully, or quant approach snapped us back into the market in time).

By the time a discretionary committee would have given the all-clear it was too late to catch the best part of the rally from the April lows.

With CTA/momentum already max long, if the market rally continues it will likely be because discretionary institutions finally pile back in.

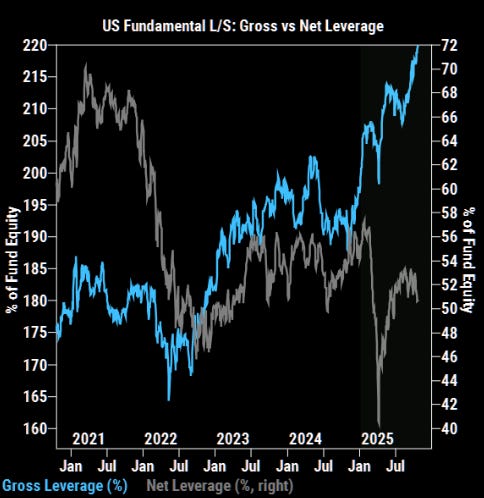

Gross exposure is up, but net exposure is low, which means there is heavy short interest across the market.

Hard to be a bear

With the mass quant buying behind us, the next big CTA move will be mass selling. So the sword of Damocles hangs above the market.

But at the same time US GDP is strong - boosted by a massive capex build out - inflation is mild, and there is likely going to be a rate cut this week.

So it’s not clear. But healthcare, which performed well in the dotcom bust, is in a far earlier point in its cycle. Which is another reason we’re focussing our attention there.

Best regards

Michael