Dear investors and well-wishers,

The fund returned -6.5% in November, which took us to +37% net for the calendar year-to-date, which is in line with our last three year return of 37% net per annum.

This was a period where there were significant drawdowns in speculative areas like quantum computing, nuclear, neoclouds, and space, though there has been some recovery in December, mostly in defence-related names.

Some years there are many ways to make money - this was one of those years where the path was narrow.

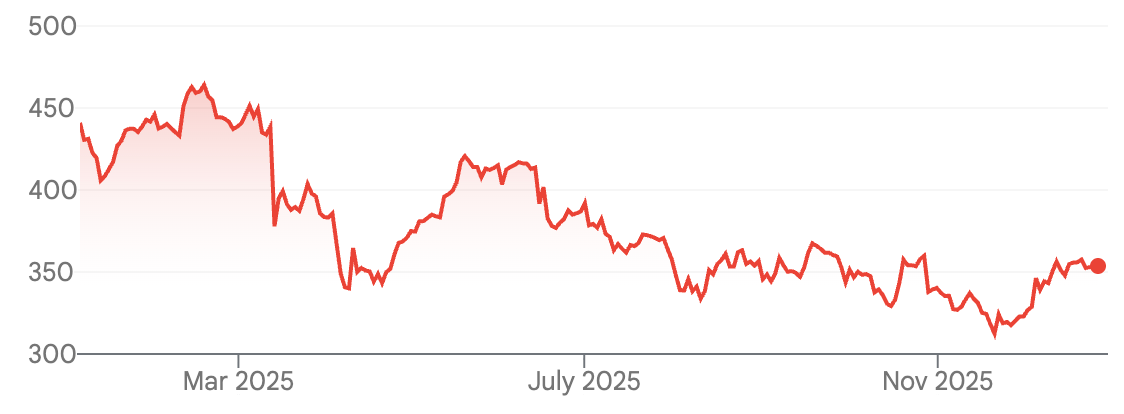

Aussie tech indices are down 11% ytd:

And a quick look at the holdings explains why:

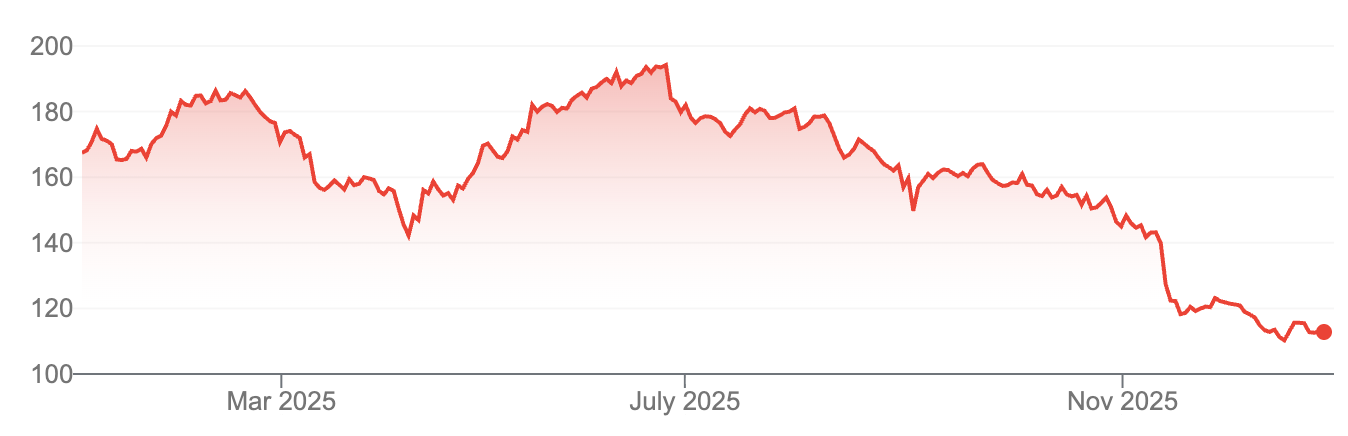

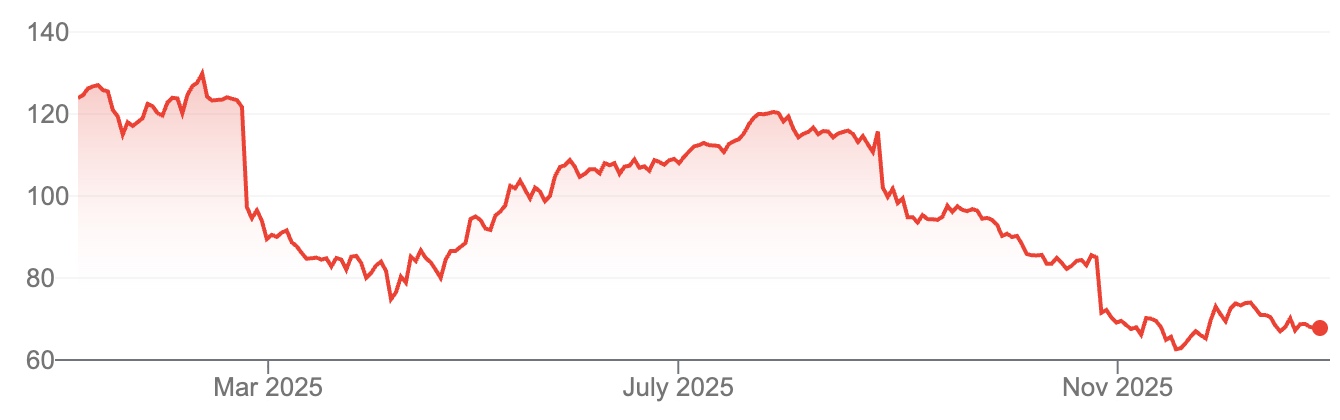

Xero stumbled, down 33%:

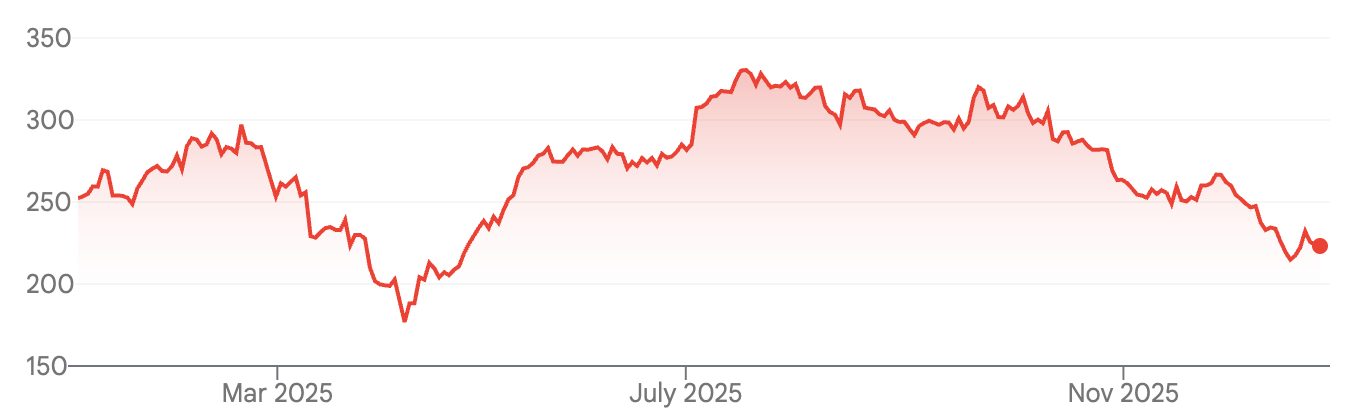

Wisetech had well-publicised issues, down 45%:

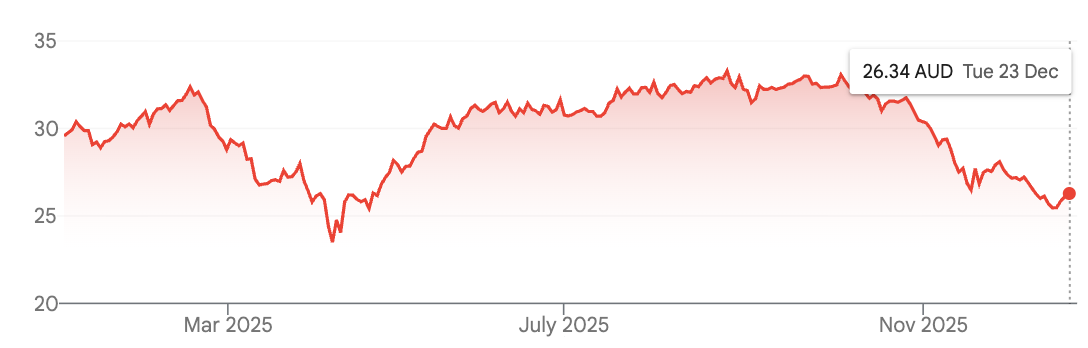

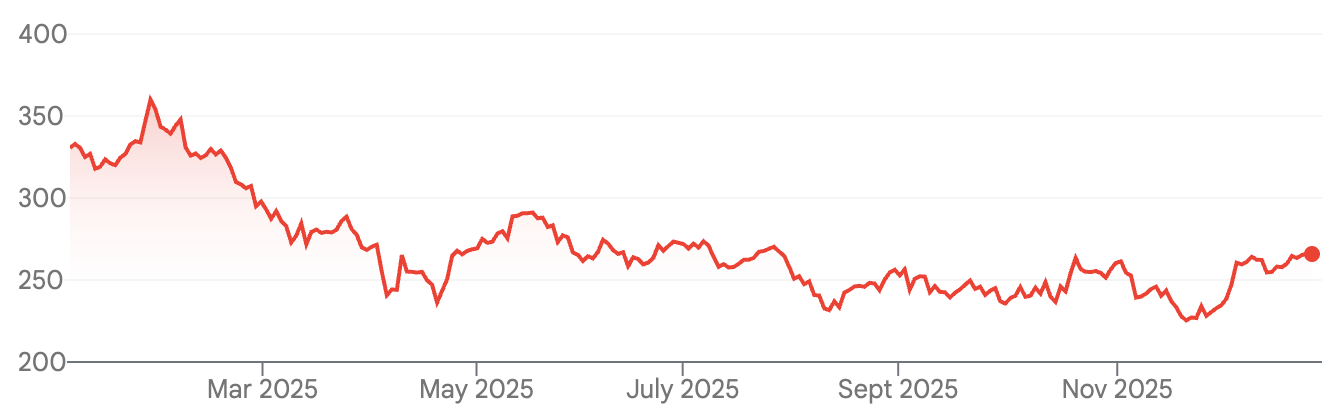

Pro Medicus has had a rare negative year, down 12%, though it’s still on 110x revenue:

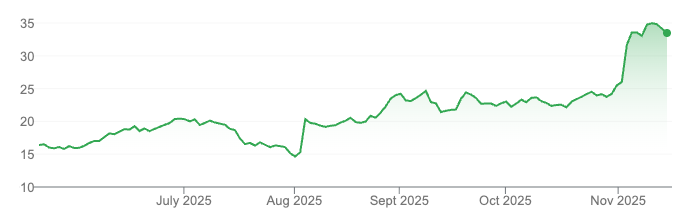

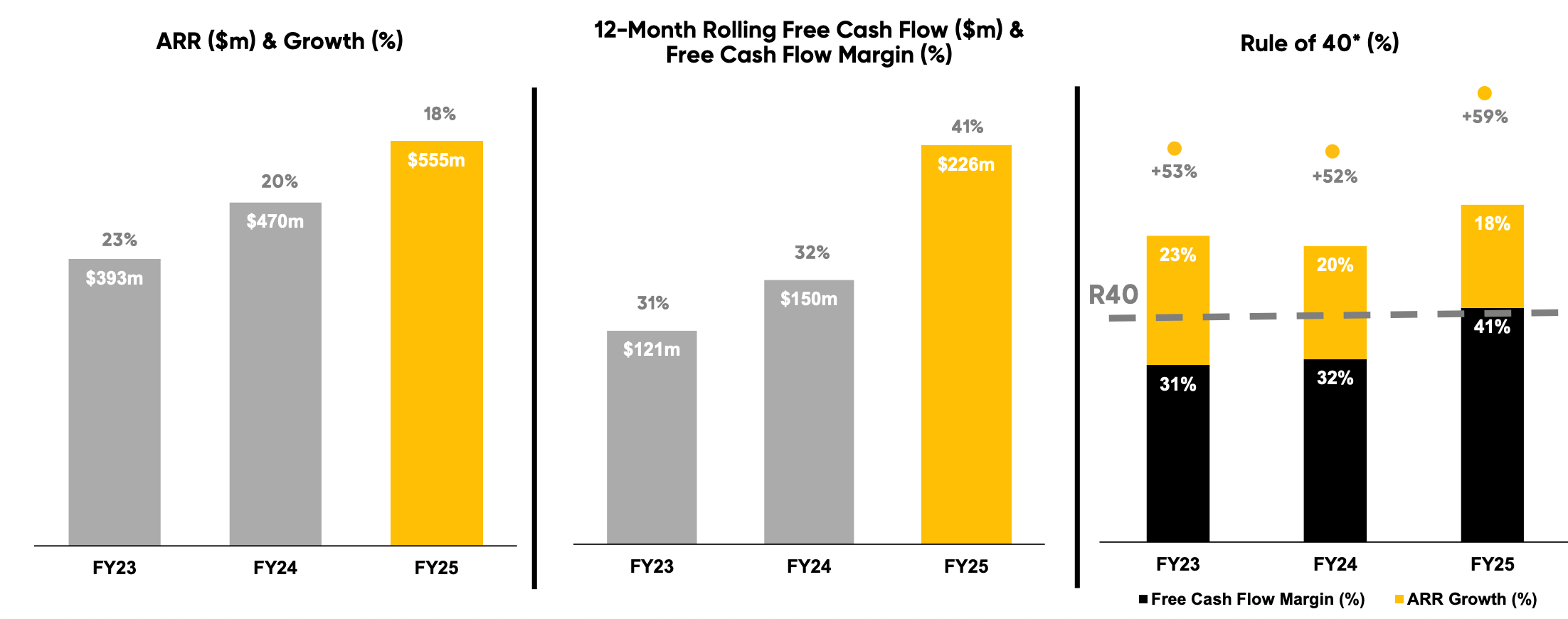

There were others too, like Technology One, down 9%:

Though results have been solid, so a decent multiple contraction this year:

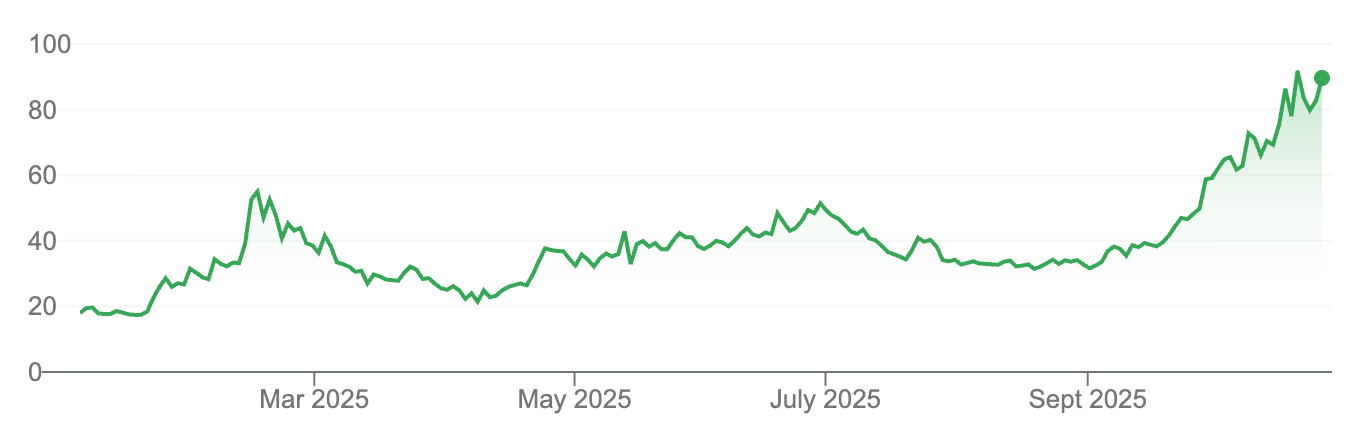

More recently Life360 joined in the sell-off, though it’s still the top performer of the group, up 48%.

In past letters I’ve noted that Aussie growth stocks counted amongst the most expensive in the world, perhaps because growth stocks of scale are few and far between on the local exchange. This was the year where those valuation multiples compressed.

Perhaps Australian companies were taking the lead from the US, where software was another area of weakness, with cloud indices down for the year:

With notable weakness in companies like Salesforce down 20% for the calendar year:

Adobe, also down 20%:

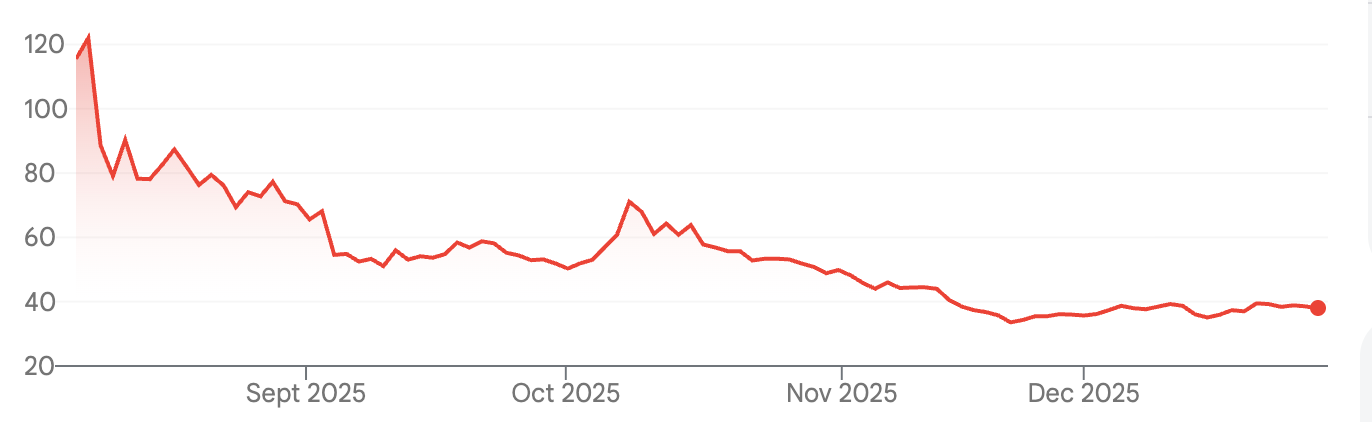

And of course Figma landed heavy losses to whoever bought the IPO pop at <$120:

I could give more examples, but it’s clear the market is moving hard away from legacy software and towards AI beneficiaries, which now include heavy industry and energy companies that were quick to pivot.

The latest generation of models (a few weeks ago) showed the biggest step forward since the launch of ChatGPT

I left the development of our internal tools to software engineers this year, but with all the hype around Claude Code I had to try it for myself.

And I’m glad I did, because it was one of those step-changes in performance and UX that you have to experience to believe. I’ve long-wanted a diary app that has features missing from current generations - the ability to interact via email, integrate Photos, have smart prompts to help build content out and get those memories down on paper.

Claude one-shotted this app in a few minutes.

The most impressive part is that I didn’t write or directly edit a single file, the whole thing was built through text in a terminal. All of a sudden it looks like development tools like Cursor, and preGPT tooling like Intellij (which used to be one of my larger non-financial subscriptions at ~$1000/year) seem irrelevant, as the experience is better in a terminal app. If you asked me a year ago I would have guessed the world moved in the opposite direction.

The best coders are waxing lyrical:

Andrej Karpathy@karpathy

I've never felt this much behind as a programmer. The profession is being dramatically refactored as the bits contributed by the programmer are increasingly sparse and between. I have a sense that I could be 10X more powerful if I just properly string together what has become

4:36 AM · Dec 27, 2025 · 14.8M Views

2.49K Replies · 6.98K Reposts · 53.1K Likes

DHH@dhh

Opus, Gemini 3, and MiniMax M2.1 are the first models I've thrown at major code bases like Rails and Basecamp where I've been genuinely impressed. By no means perfect, and you couldn't just let them vibe, but the speed-up is now undeniable.

4:13 AM · Dec 28, 2025 · 318K Views

125 Replies · 136 Reposts · 3.25K Likes

Now that these tools can operate on their own the compute demand is going to be astronomical. Their ability to handle larger and larger codebases is only going to increase. It feels like ‘God of the Gaps’ as the space that LLMs can’t operate effectively shrinks with every new release.

This is excellent news for AI infrastructure. There were fears only a few weeks ago that progress had stalled, but with these updates it’s now far more likely that demand will match or exceed the upper end of estimates next year, with significant relevance to the investment world.

Some software will be in higher demand than ever - namely services you integrate into an app - while other tools like image generation and certainly website building will lose customers to the LLMs which can operate fine on their own. It’s obviously a win for hyperscalers and Nvidia.

And it’s not just code. Self-driving Waymos have been taking significant market share in San Francisco and other US cities all year. Late next year or early 2027 they will start to do the same in Australia too. Sometimes it’s easier to pick the losers than the winners.

On that point, there’s an interesting debate over whether Uber will aggregate demand and be the consumer layer to multiple underlying self-driving companies, or whether Waymo, Tesla etc will develop their own networks. We have no financial dog in the fight, but are watching as these shifts can generate monetisable trends.

Aggregation theory is pretty well understood now, courtesy of Ben Thompson. Companies that aggregate customers end up eating alive those that hand them the customer relationship. Waymo and Tesla have invested enormous sums building self-driving tech, so I doubt - at the finish line no less - they’d hand over the customer relationship to a third party.

And where does this leave the Figmas et al? This is another debate that will only be settled with time, but having seen the power of the base models, and their improvements in UX, I suspect more and more workflows will happen in their environments directly.

Bulls can point to software’s long history of creating user-friendly skins, and value accretion to platforms which provide a better user experience in a particular area, even if they’re built on top of the general tools.

The amount of software being built is going to accelerate dramatically.

But the competition for customers will be stiffer than ever. So the ability to create and maintain an audience will become critical, and the competition for attention is going to be fierce. The stakes are also increasing, as previous bottlenecks vanish (like the ability to build complex software).

It’s also made me pause and wonder whether I’ve been too bearish on foundational models. These aren’t listed and we aren’t invested directly in any of them, but global datacenter capex (and now global GDP growth) depends on their success.

For most of this year I’ve assumed there was an impending bloodbath, as cheap open-weight/open-source models fought it out with the early incumbents for market share. Especially once Google - funded with enormous cash flows - began to compete and use their LLMs as well-funded loss-leaders.

That might still happen, but the argument is less convincing now. If you’re using ChatGPT as a chatbot, there’s little downside to using a free Chinese model hosted on Amazon or Microsoft. But giving that Chinese company full access to your computer, servers, etc? Absolutely not.

That power could only be trusted (if ever) with the largest companies in the West, who have the most to lose if something goes wrong, and are being closely watched by the entire internet.

So maybe instead of foundational models competing each other’s margins down, we get yet another positive demand surprise, and that’s bullish no matter how you cut it (or how they choose to account for depreciation, which is the core of a different bear thesis).

It’s a retail market

One feature of this year was the outperformance of retail/speculative stocks, which along with semis, big tech and healthcare, was one of the ways to outperform.

That’s cooled for now, but it’s safe to predict flows will continue to be powerful in both directions. Which isn’t saying much (stocks will go up or down!) but most of the market doesn’t flip from exuberance to depression and back multiple times a year, so a traditional approach is not going to work here.

This is one of the areas where our quant approach works best.

The impact on the investment world

In the investment world it’s increasingly clear how a handful of quant/tech-first firms are harvesting so many billions of dollars out of the active manager pool every year, and why discretionary investors are struggling so much (quant profits have to come from somewhere).

If a handful of firms are going to capture the lion’s share of profits, and quants are going to capture a chunk more, then the outlook for active managers is bleak.

Of course, there is an active choice: don’t fight these forces, but join them, and back these trends. Prices are certainly going to move.

Healthcare is blissfully orthogonal to these debates

One trend I expect to continue is the performance of fast-growing revenue-generating healthcare companies - a sector which is safely independent from disruption elsewhere. This is currently more than half our portfolio.

In the fund, we’re positioned in a combination of fast-growing healthcare names and beneficiaries of computing demand (with a few independent growth stocks thrown in), all managed with our proprietary risk systems. And that looks like decent positioning for 2026.

Thank you for your trust and partnership. Wishing you a relaxing break - please reach out any time.

Michael