Dear investors and well-wishers,

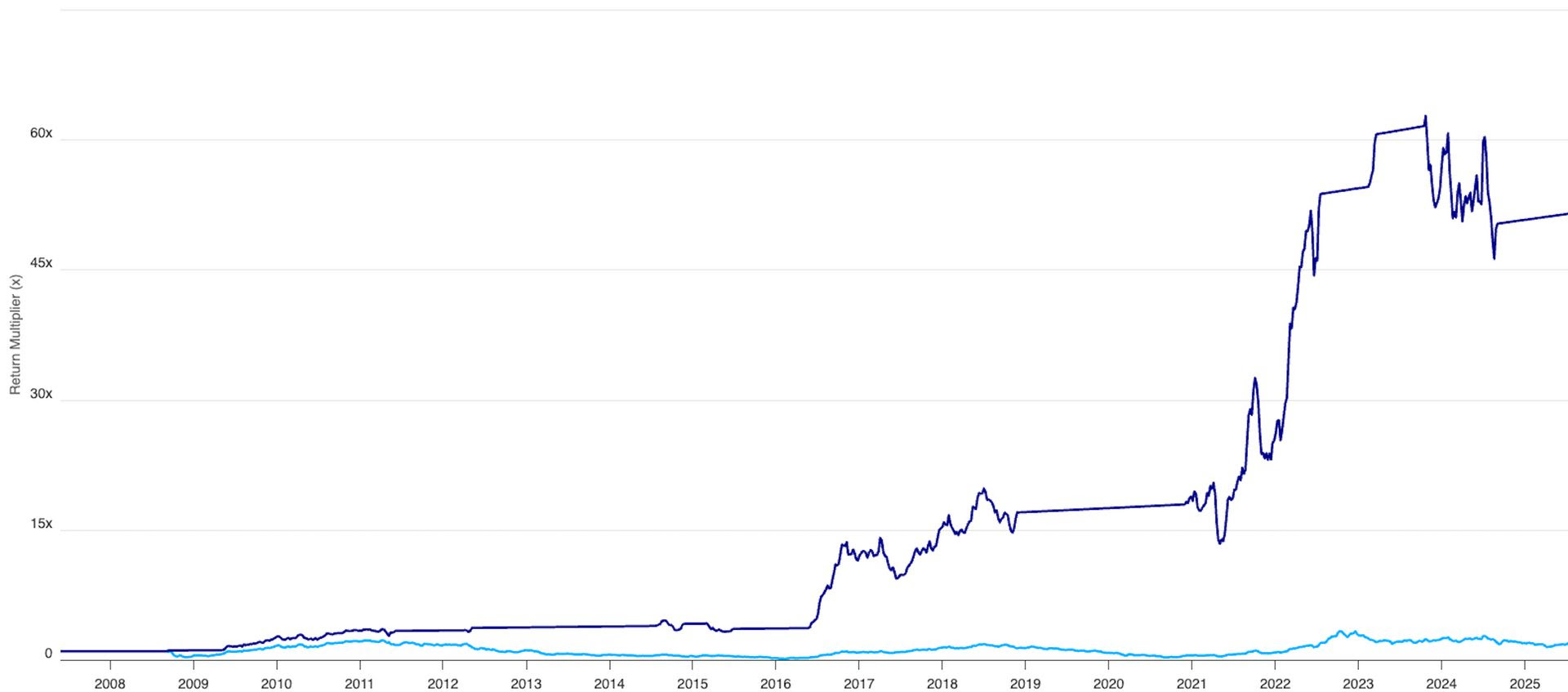

The fund advanced 24.5% in June, and we are now up +30% net for the calendar year-to-date.

If you’ve heard me talk about markets over the last two years you’ll know how excited I’ve been to apply our AI risk models to growth stocks. But even so - it was impressive to watch them move the portfolio to 50% cash and then aggressively buy back into growth stocks near the lows shortly after.

Semiconductors

We flagged that the semiconductor sector was a space to watch, and it has led the market in recent weeks. Semiconductors (and healthcare) are still below their peaks last year.

We were out of the sector for most of the year, which is a strange way to invest in a sector we’re so bullish on. But it worked, and we were beneficiaries of the latest rally.

ChatGPT is quickly becoming the front page of the internet for many, and for most queries it’s substantially better than Google’s ads and SEO-gamed links.

There’s a huge amount of noise around peaking datacenter capex, but here’s a signal straight from the source, posted by Zuckerberg two days ago:

For our superintelligence effort, I'm focused on building the most elite and talent-dense team in the industry. We're also going to invest hundreds of billions of dollars into compute to build superintelligence. We have the capital from our business to do this.

SemiAnalysis just reported that Meta is on track to be the first lab to bring a 1GW+ supercluster online.

We're actually building several multi-GW clusters. We're calling the first one Prometheus and it's coming online in '26. We're also building Hyperion, which will be able to scale up to 5GW over several years. We're building multiple more titan clusters as well. Just one of these covers a significant part of the footprint of Manhattan.

Meta Superintelligence Labs will have industry-leading levels of compute and by far the greatest compute per researcher. I'm looking forward to working with the top researchers to advance the frontier!

Mark Zuckerberg, posted on Facebook 15 July 2025, emphasis mine

The few titans running hyperscalers are all determined to stay at the forefront, and that means datacenter capex will continue, along with outsize orders for everything from Nvidia GPUs to base power and cooling.

Nvidia has been the easiest way to invest in AI, but there are a number of higher returning opportunities in smaller companies that are growing faster than the sector.

Many of these dropped 65-75% only a few months ago, offering helpful entry points into companies we might otherwise have been missed.

We’ve been lucky that this market has been a good match for our risk-managed approach, which benefits from outsize moves in both directions. We basically had a full cyclical crash and recovery in less than six months, reminiscent of COVID crash and recovery five years ago.

US tech has been an outsize performer for us, while healthcare has lagged.

Fortunately, biotech is now finally catching a bid off an extremely low base, and if the recovery continues in the second half of the year we are positioned to take full advantage.

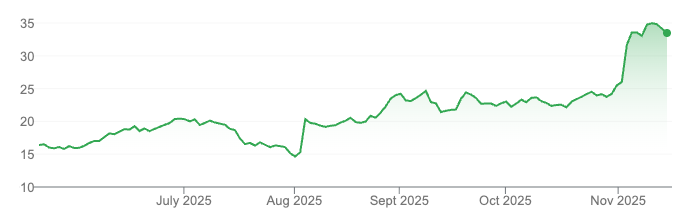

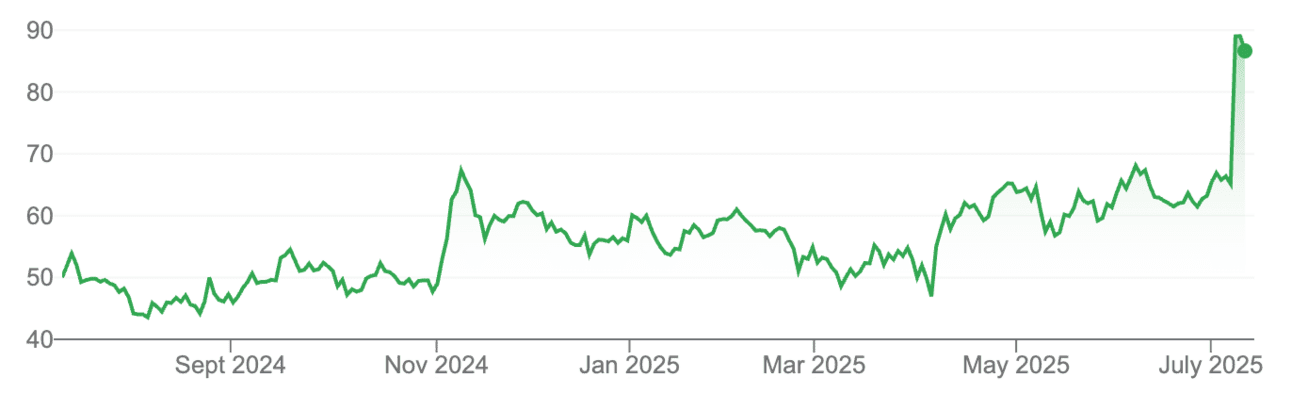

Clarity Pharmaceuticals

I wrote that Clarity stock was in a classic momentum unwind, where higher prices attracted more buyers, and subsequently, lower prices attracted more sellers. Once a stock starts trading like this it often continues, as heavy short-selling and waxing and waning retail demand creates outsize moves.

Fortunately in momentum unwinds the fire eventually burns out, and the price reaches a level that no further investor will sell at - which creates an opportunity. In April we bought steadily for an average of $1.69.

Clarity is one of those companies where serious revenues would come in 2-3+ years, and these were discounted to oblivion when investor timeframes shrank from years to months. But as we move into the back half of this year and into next year, all of a sudden 2027 doesn’t seem so far away.

Buying some $CU6 today - going to test if this biotech liquidation has run its course

Earlier this month Cannacord hosted a call with Dr Oliver Sartor, one of the global leaders in prostate cancer. At the end of the call the conversation turned to Clarity.

There’s about a million men in the United States with high PSA, and a significant number of those, perhaps 600,000, test negative on current screens. That’s a large population that knows they may have a problem, but doesn’t have enough diagnostic information to guide treatment.

These patients are in a difficult position. Dr Sartor had one patient willing to fly to a different state to access Clarity’s diagnostic, and if it was unavailable there, was prepared to fly to Australia.

I’ve had conversations with investors and fund managers who are intensely sceptical that a new company could take on such entrenched incumbents. But this isn’t a consumer product, Clarity’s not making smartphones or cars.

Those at risk won’t just prefer a better diagnostic, they’ll insist on it.

Clarity has now more than doubled from the lows, but remains a long way (nearly 150%) from the peak last year. You can see our interview with Executive Chair Alan Taylor here, and our interview with local KOL Professor Louise Emmett here.

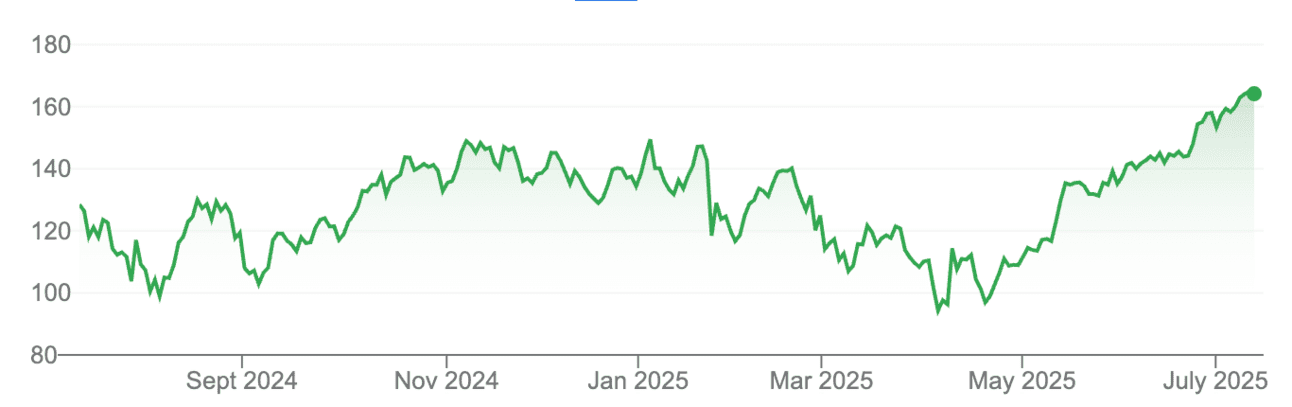

Rhythm Pharmaceuticals

We invested in Rhythm Pharmaceuticals, which treats rare forms of obesity caused by injury, cancer, or genetics.

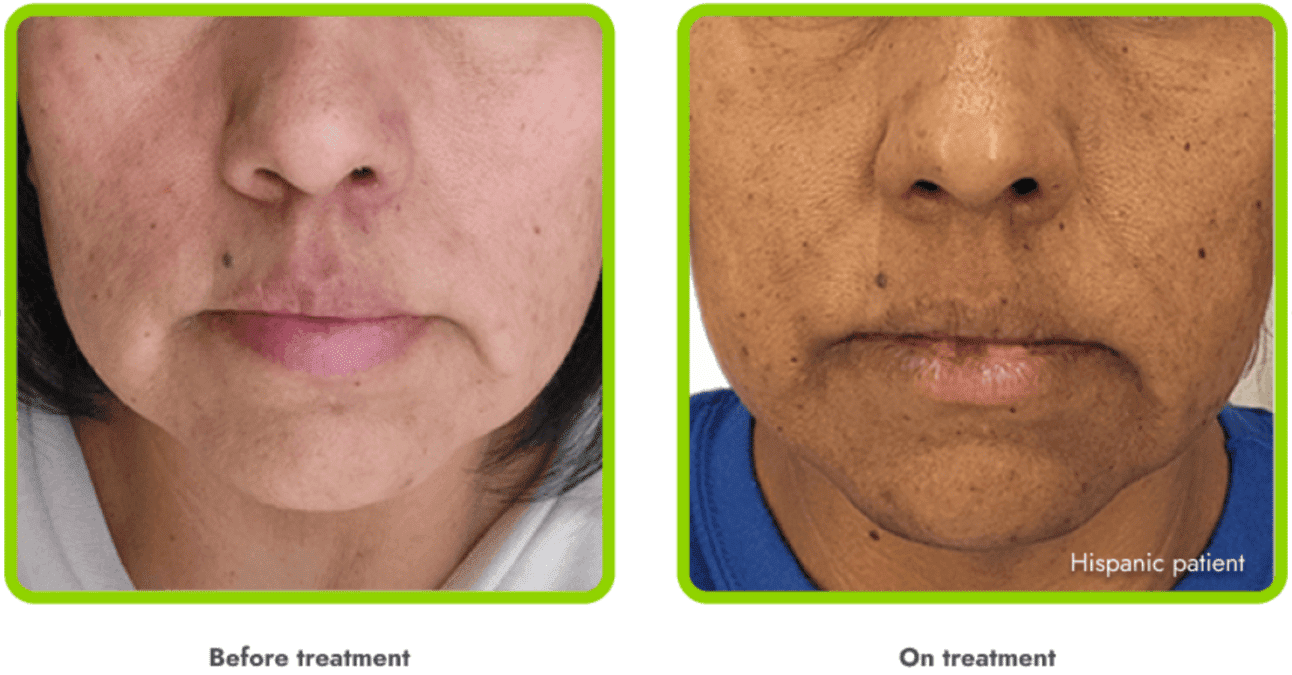

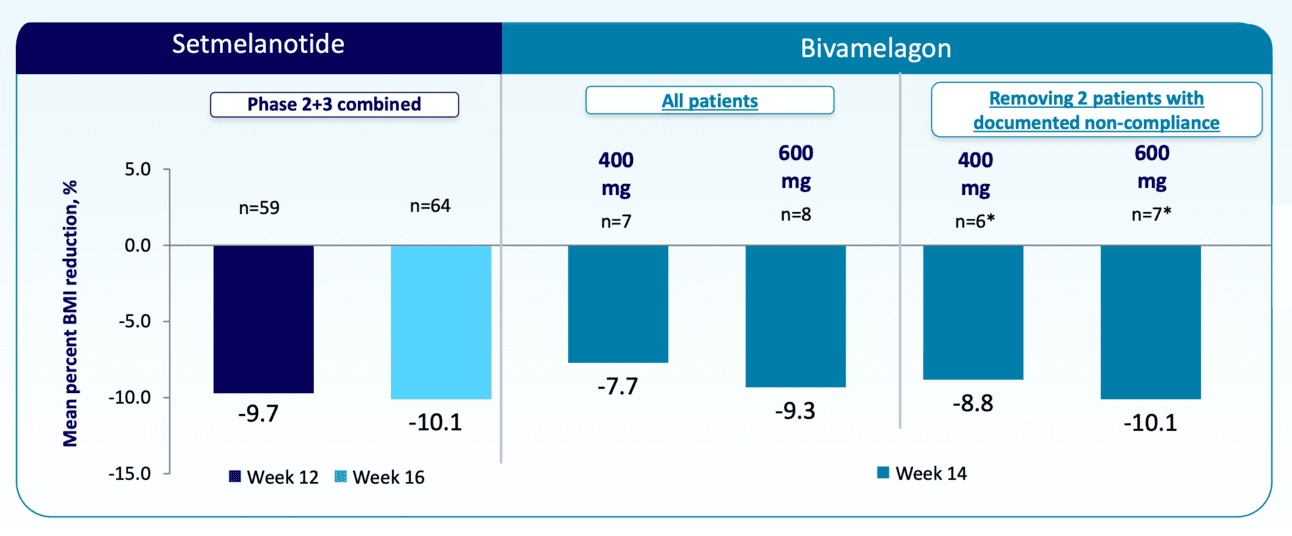

Rhythm is annualizing ~US$150m from their existing drug setmelanotide, but this comes with the unwelcome effect of hyperpigmentation.

The company’s next generation drug targets the same mechanism with lower side effects. Data released last week shows robust, dose-dependent weight loss, comparable to the first-generation drug, but with more limited hyperpigmentation.

A better solution expands the company’s potential market, and the stock reacted accordingly. At a market cap of US$6 billion, we think this is a well-differentiated buy-out target for big pharma companies who have missed the boom in obesity meds (which is most of them).

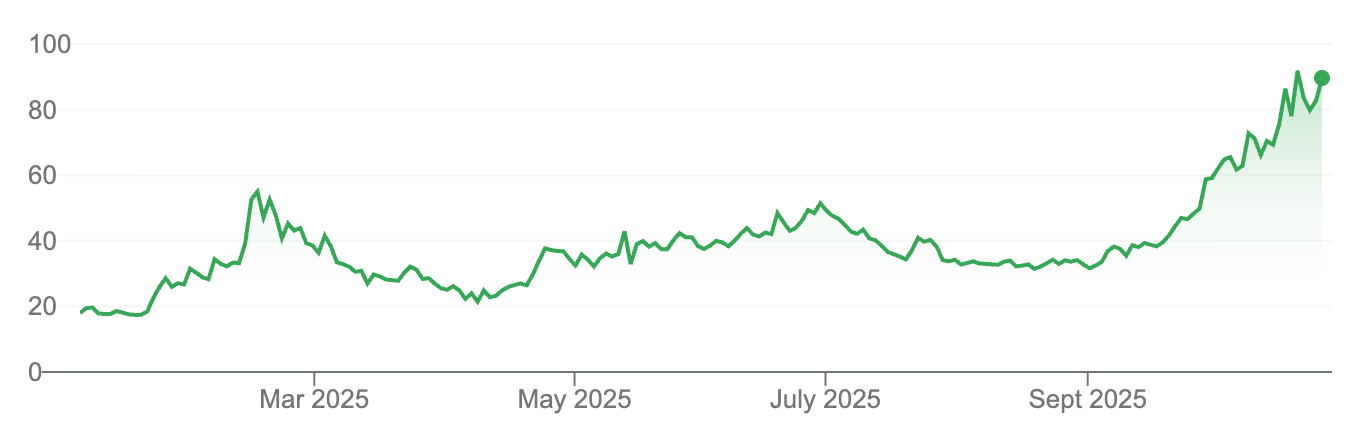

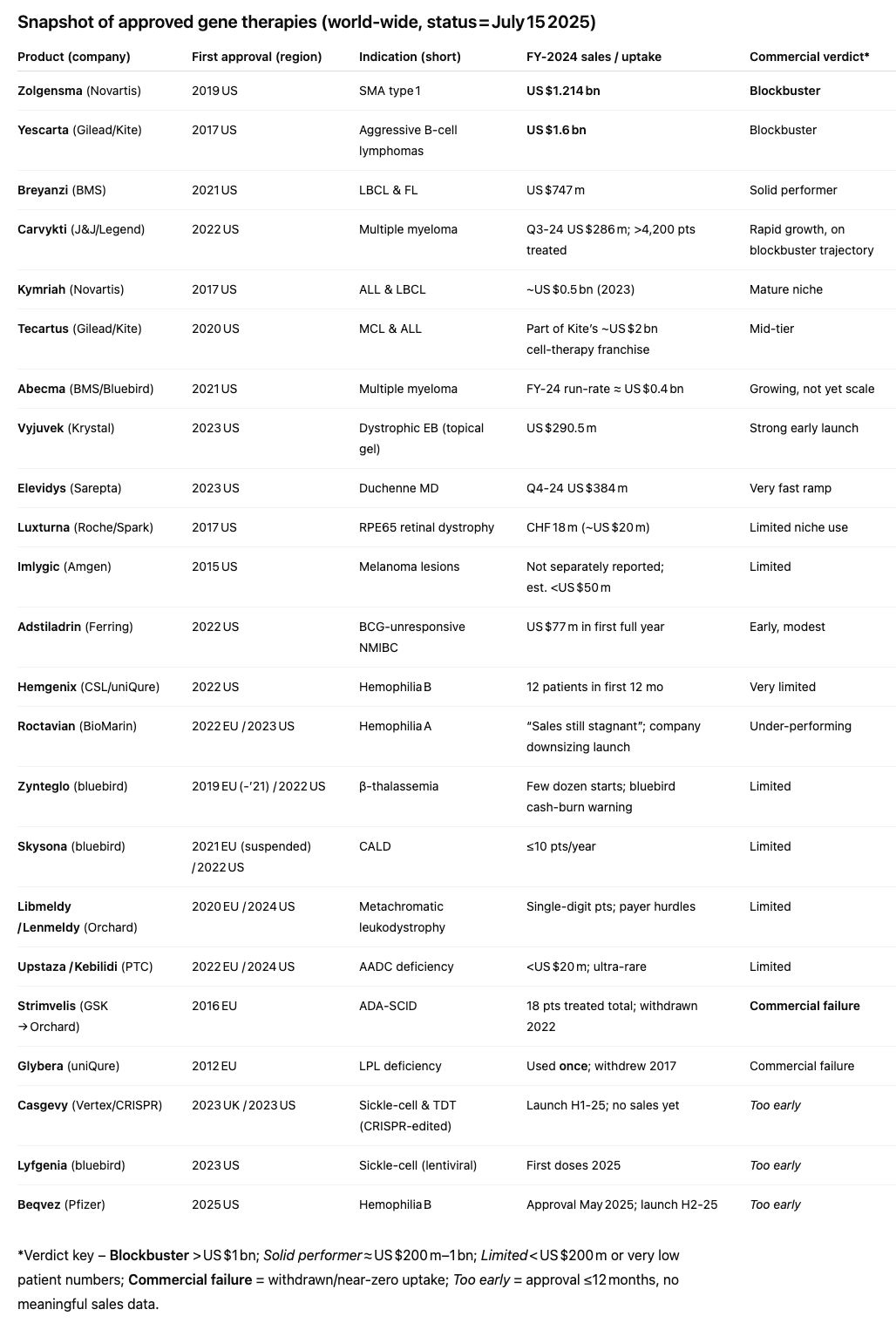

Gene editing companies - is the suffering finally over?

We’ve taken another look at this once hot part of the market, which has been selling off more or less consistently since 2021. Long term readers will know I’ve been a sceptic due to the immense cash burn of leading companies, and the fact they’re mostly targeting competitive spaces.

Most approved treatments have been commercial failures, and have very different commercial dynamics to small molecule drugs, which are at least extremely cheap and profitable to manufacture once approved.

For all the investment in these companies, there have only been two blockbuster successes so far.

But, for the first time in years, perhaps the sector might now perform. Clinical programs have matured, prices are lower, and our risk models which proved so powerful in tech have just flipped from sell to buy. These same models saved us from temptation during a long bear market.

This approach is also powerful in commodities. Out of curiosity I applied one of our models to hot-topic companies like Mineral Resources and Whitehaven Coal.

ACE Venture

Our software development studio now has over 25 engineers and we just hired again in Australia. If you want to explore an idea reach out and I’ll put you in touch with our CTO. Ace has been instrumental in building out our own AI systems.

We’re investing heavily in our own capabilities and infrastructure. In funds as with companies, there will be a sharp dispersion between those that make full use of the new AI toolkit, and those that don’t. Even long established quants will have to adjust - traditional momentum and vol targeting funds seem calibrated too slow for the current market. They certainly were this time around anyway.

ROAR

We’re anticipating a late August/early September launch for our ETF (ticker ROAR). The ETF will focus on >$1 billion listed growth companies and will have significant overlap with our existing fund.

It will sit lower on the risk/return spectrum than our existing fund, and won’t (for example) include early stage biotech or small caps. If you want to be kept in the loop please let me know, and we’ll organise meetings and events once we have a firm launch date. I’ve kept track of everyone who’s expressed interest so far.

Outlook

We began harvesting profits in US growth, though we still hold the bulk of our exposure.

Earlier this year algorithmic funds systematically sold hundreds of billions of dollars of equities, and those same funds are now buying.

By at least one measure, the wall of money hitting the market this July is higher than ever.

Things will get harder from here. At best, markets are two steps forward, one step back, and as we move into earnings season there will almost certainly be more dispersion and greater divergence in outcomes.

Parts of the market are turning red hot, especially in the United States.

But at the same time, other sectors like healthcare, and arguably broader semiconductors are at the earliest stage of recovery (putting Nvidia aside, as it’s is basically it’s own separate category now). We will be watching these sectors closely for outsized opportunities.

Best regards

Michael

If you'd like to invest with us, you can access our investment portal and fund documentation through the button above.

If you’d like to speak to us about opportunities with our venture studio reach out using the link below.