Dear investors and well-wishers,

The fund returned -14.7% in March.

We had a large amount of cash as our risk model cut almost all our US tech and growth positions.

However, we kept around 40% in biotech, and after the Opthea collapse and the US biotech sell-off these all sold off >50% from February, though there has been a decent rebound from the lows in mid April.

It’s an exciting time though, as we found ourselves with our largest cash balance in years, and a number of high quality growth businesses were down 40-65% in just a few weeks, which gives us a clear path for a strong rebound.

In mid April we deployed some of that cash, doubling our position in Clarity, adding to Anteris, buying back HIMS, and taking new positions in Rhythm Pharmaceuticals, Byrna and InteractiveBrokers.

Biotech

Clarity has now bounced ~40% from mid April, read our latest note for a specific update.

There was significant shortselling at the lows, which will now be significantly under water. Short sellers will have to hold through the read out from their head-to-head trial, the first of two Phase 3 readouts in diagnostics, and updates from their dose-optimised therapy trial. Clarity is tackling two $10 billion markets, so the main bear thesis arounds when and at what price they’ll raise the money to tackle this opportunity.

We picked up some shares at the low at 1.45, and roughly doubled our position at an average of 1.70 in April.

Anteris has developed a new kind of heart valve that has now been used in over 100 patients in some of the United States’ leading medical centers. We’ve discussed the product with a number of surgeons who use it - and their references are glowing.

Anteris’s transcatheter heart valve

From late February to mid April the stock dropped nearly 75%, from $8.8 to $2.3, and this was not a small position. There was a recovery in the last week or so. We purchased most of our shares in their US listing at $6.

I recorded a podcast with the CEO Wayne Paterson last week, and will release it shortly with some commentary.

The company has $1.8/share of cash, and we added at around $3.

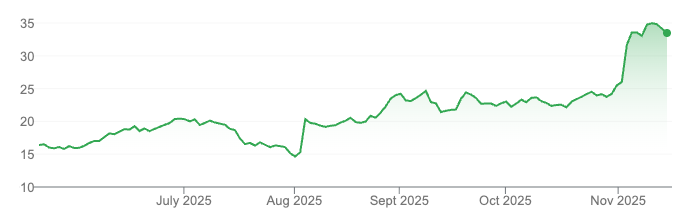

Anteris Nasdaq-listed stock price, currently $5.5

Syntara has a major readout in June. This will show a more complete dataset from their myelofibrosis trial after an extremely positive interim update in November last year. This is another stock that is materially undervalued relative to its opportunity at $88 million market cap with $18 million of cash.

United States growth tech

Hims&Hers

HIMS peaked at $73 and sold off to $25 in this period, a 67% drawdown. The firm reported revenue growth of 69%, and 45% growth in customers, and is continuing to perform strongly.

Yesterday they announced a partnership with Novo Nordisk to offer branded Ozempic on their platform for US$599/month. Both Eli Lilly and Novo are experimenting with going direct-to-consumer, and the partnership is a significant win for the company.

There were questions around HIMS ability to source product once GLP-1s were taken off the FDA’s shortage list, which meant they were no longer allowed to use cheap compounded versions. This announcement resolves that issue, which was the primary overhang on the company.

The positives are immense - telehealth is clearly the preferred customer solution (beats going to a GP), and HIMS is taking market share in a rapidly growing field. Owning the customer allows the company to cross-sell their many product lines. This is now a ~7% position.

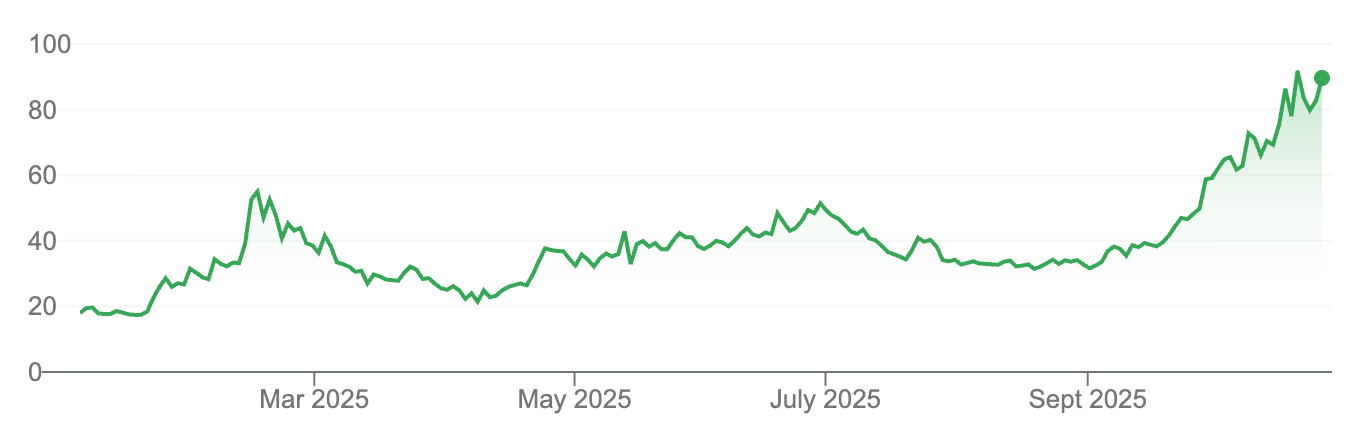

HIMS stock price - 66% fall and partial recovery. After taking profits earlier in the year, we re-entered in April

Byrna

Byrna sells non-lethal weapons which shoot painful projectiles and tear gas to deter attackers (you can actually purchase them in Australia).

We track around 150 US growth stocks across consumer, tech and healthcare, and Byrna has been on our radar for a while, so we were excited to see it fall 60% over a period where it reported strongly.

Byrna stock price

Byrna announced revenue growth of 57% organically and are GAAP profitable, with expansion opportunities in-store and online. They benefit from rising concerns over crime and the desire for protection that doesn’t risk a murder charge. They manufacture the bulk of their products in the United States, so are largely immune to tariffs. We initiated a ~6% position at $19-20 in April.

Rhythm Pharmaceuticals

Rhythm Pharmaceuticals a drug for weight loss (setmelanotide) that operates via a different and complementary mechanism to GLP-1s.

Unlike GLP-1 competitors in the market, they target weight loss caused by specific diseases.

A few weeks ago Rhythm announced a successful Phase III trial readout for weight loss in hypothalamic obesity, where the hypothalamus is damaged by tumors, tumor treatment, or injury.

This led to ~20% weight loss, and 25% when used with GLP-1s. In a different market the stock would have ripped.

The drug is already on the market for Bardet-Biedl syndrome, generating US$42m revenue in Q4 last year, up 26% on the quarter. This new approval increases their commercial opportunity by 2-3x. Combined with a potential approval in congenital hypothalamic obesity - which I see as likely given their prior success - this would ~10x their revenue opportunity.

With almost every major pharma co looking to enter the weight loss market, Rhythm is differentiated in its mechanism, in its strategy targeting specific diseases, and carries lower overall risk as their drug is already on market generating revenues.

Rhythm is likely a highly attractive takeover target, particularly as so many GLP-1 contenders have fallen short of Eli Lilly’s Mounjaro and next generation assets.

Interactive Brokers

It’s true that the best investments have been right in front of us. You probably have an iPhone in your pocket and might be reading this on an Apple computer. Google, Facebook, Microsoft, Spotify are all part of our daily lives, and have been powerful performers in the market.

Interactive Brokers is one of those platforms that we should have bought long ago.

It’s vastly cheaper than alternatives, and while less friendly than some consumer platforms, is vastly easier to use than institutional alternatives (trust me).

IBKR dropped 44% from Feb to mid April, along with everything else in our universe it seems, and this was high on our shortlist, so once momentum recovered we took the opportunity to buy it for the first time.

Operating income grew 21% year-over-year, but customer accounts, the real driver of value, grew 32%, with commission revenue up 36%. Margin revenue only grew slightly as the entire market seemingly reduced exposures across the board.

Management has been extremely cost-focused, and years of investment in infrastructure allows them to offer functionality at a price that would be extremely difficult to replicate.

IBKR is growing slower than our usual >50% portfolio companies (and there are plenty of those who were cut in half or more since February) but on a forward PE of 22x, and plenty of customer love, this is one we really wanted to own. There’s also an element of counter-cyclicality as trading volumes increase at times like the last few weeks.

Outlook

Had we only invested in US growth, this would have been a highly successful period, as our losses in that space were minimal.

We had a high weighting towards biotech, and as major funds exited the market in Australia, there was an indiscriminate liquidation. In the future we’ll have lower weightings to the sector, but this is a time for buying, not selling.

There was a similar moment in 2022, where half of US biotechs traded below cash. Roughly 60% of all drugs developed come from the biotech sector.

We’ve observed before that platform companies didn’t recover, but the companies that succeeded in pushing their drugs through the pipeline often rebounded 5-10x in very short order. At the highs, upside was 2-3x. After moves like this, the return opportunity is an order of magnitude higher, especially in cases where companies trade close to cash, as we saw with Anteris.

So we have high confidence in these companies, which could alone return the fund in the mid-term.

But the real exciting opportunity is actually in growth tech. Along with those above, we have a long list of companies growing over 60% which had 65% drawdowns in this period, and are now trading at the cheapest they have in history. In the past we would have just bought, but we’re going to be disciplined and add only when our risk models give the all clear. We’ve already added the first to recover - like Byrna, Interactive Brokers, and HIMS, and will now wait and see.

There’s a scenario where markets deteriorate further and we raise cash again - though it’s helpful that algo/quant market has flipped from long to short, and hedge funds have significantly degrossed. That part of the move is behind us at least, and at some point, will lay the ground for a 12+ month bull market.

If markets continue to recover we’ll add to companies like Reddit which fell 65% which posted revenue growth of over 70% and significant growth in cash flows, while falling 60% in the market.

Michael