Dear investors and well-wishers,

After a 25% April, our wholesale fund had a similar return in May.

Towards the end of the month we made a major quant-driven shift into software, which is now one of our largest holdings.

The AI-decline thesis was always a narrative. The 50-80% falls were driven by fears of AI-disruption fears, rather than something that showed in the numbers.

For the software sell-off to continue, you would expect shocker reports from SaaS companies to filter through this year at each earnings season.

So far, with some notable and (arguably avoidable) exceptions, that has not happened. In fact, a number of companies have actually accelerated.

This means the prevailing narrative is at odds with reality, and there’s an opportunity for a major market move. Perhaps even a regime change.

Positioning makes this particularly interesting.

Fund management exposure to semiconductors has rocketed from the lows in 2023, which combined with retail momentum and all kinds of weird, wonderful and popular leveraged instruments, made this the best performing sector (of which we were certainly beneficiaries at various times).

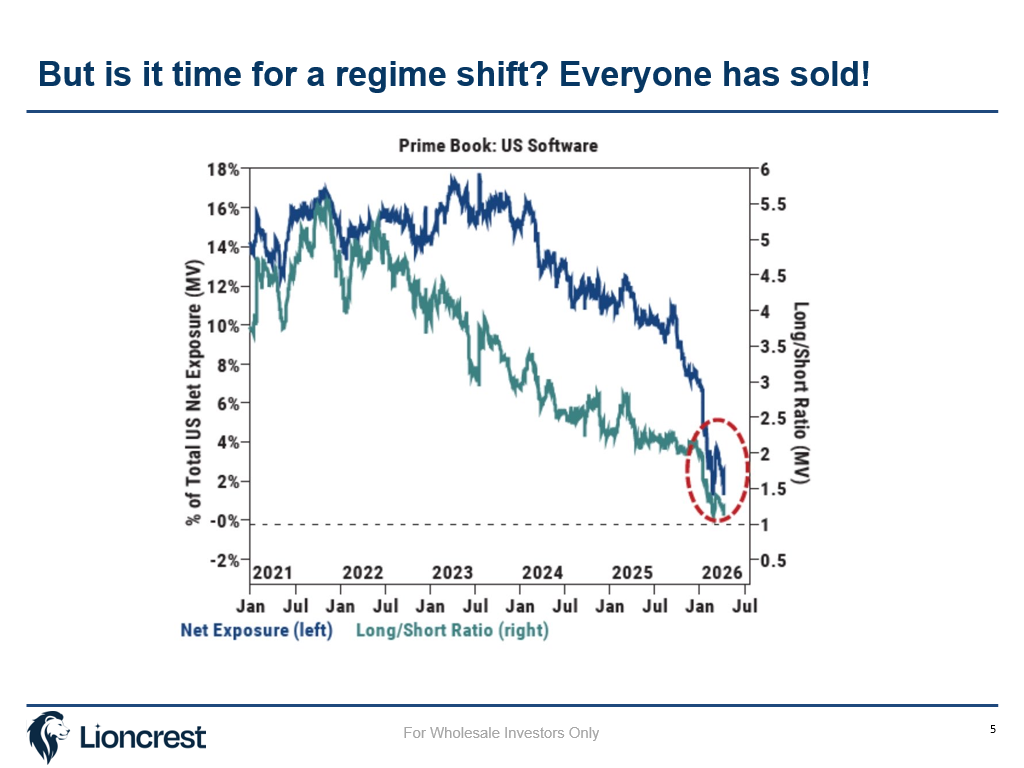

Now we have a curious situation where software is basically not owned at all. What fund manager would dare admit they own Atlassian today? Ownership is basically at zero:

This isn’t just the long only crowd, funds have also piled on the shorts.

Note in the chart below, the peak of semiconductor short interest was in early 2025, and we know what happened after, semis went vertical:

Software is now at those levels.

This is now one of our largest exposures in our wholesale fund. As in May when we bought semis before a major move, we added right before a substantial rally in software, mostly in the last few days of the month. Computers are the future.

We bought across the sector, including Snowflake, Rubrik, Gitlab, Atlassian, ServiceNow, and even Figma, as well as some others.

Of course, our quant system will take us out of these positions quickly if this is another false dawn, and given the rapidly changing landscape the sector is certainly not for the faint-hearted.

Australian tech

Before my compatriots ask, it’s not clear whether this will spread to Australian software, but it might.

Aussie tech has been uninspiring, and given the substantial increase in capital gains tax about to hit Aus, the local market may be under some pressure.

Spare a thought for the local biotech and drug development sector, which is likely one of the biggest losers.

And many local software companies are challenged, each in their own way. Xero has slowed and accounting is genuinely at risk of AI disruption. Wisetech’s largest customer is building a competitor in-house, and given the pressure on consumers, companies like realestate.com.au and CAR are hard to get excited about.

So the vast bulk of our buying has been overseas, partly funded by taking profits in semiconductors that more than doubled from our purchase prices several weeks ago.

ASX: ROAR ETF launch tomorrow

We are finally launching our Lion Active ETF tomorrow, under the ASX ticker ROAR (there’s a Canadian stock with the same ticker, no relation).

This is a different strategy to our wholesale fund, with separate governance, a separate management company, a different target risk/return, and a different team, but will broadly apply the same quant approach we’ve developed over the last few years to investing in mid and large cap growth opportunities around the world (market cap over $1 billion).

We will host a webinar on Tuesday at 9am, please register here, and consult the PDS for more information. Very welcome to send my any questions or topics to cover in advance at [email protected].

Note:

The Frazis Fund operates a different strategy and risk/return profile to the Lion Active ETF (ASX: ROAR) and is available to wholesale clients only (as defined in s761G/s708 of the Corporations Act). Any Frazis Fund performance shown is that fund's history only, it is not the performance of ROAR. Past performance is not a reliable indicator of future performance and returns are not guaranteed.

The Lion Active ETF (ARSN 685 354 518) is issued by K2 Asset Management Ltd (ABN 95 085 445 094, AFSL 244 393). Offers are made only under the PDS. This is general information only and does not take into account your objectives, financial situation or needs. Consider the PDS and Target Market Determination, and seek advice from a qualified financial adviser, before making any investment decision. Investments carry risk, including possible loss of capital and currency risk. Information is current as at 31 May 2026 and subject to change.

The Lion Active ETF PDS is available at www.lioncrestpartners.com/pds