Dear investors and well-wishers,

Our wholesale fund advanced 29.6% in May, bringing our 12 month return to 85% and three year net return to 42% p.a.

I’ll host a webinar tomorrow at 9am, register here.

Please note that all returns and information in this note refer to the wholesale Frazis Fund. Our ETF, ASX:ROAR, commenced trading last week and operates a different strategy. Relevant information, including the PDS and TMD is available here.

Software

In May we made a decisive re-entry into software, which is now >40% of our portfolio.

This was driven by our quant models, but the two charts below show the scale of the opportunity.

With a few twists and turns, allocations to semiconductors have risen dramatically:

A rough proxy for hedge fund exposure to semiconductors

While software allocations have dropped from one of hedge fund’s largest exposures to close to zero:

A rough proxy for hedge fund exposure to software

Short interest in software has also reached extreme levels, similar to where semiconductors were roughly 18 months ago before their historic rally:

Short interest in semis and software

Last Friday, in a broad tech sell-off, software was surprisingly resilient. Without drawing too much from a single day, that was certainly notable shift and perhaps indicates the start of a new regime.

When positioning is this one sided, the market often moves in the path of maximum pain… which right now would be a semiconductor sell-off and a software rally.

Importantly, this shift was not discretionary. It was driven by our quantitative risk and allocation framework.

We’ve now made a number of these major allocation moves over the past few years, notably building a large cash balance three times, only to buy back into semiconductors right before major moves. We also sold software many months ago, avoiding a significant sell-off that caught out professional and retail investors alike.

And now after a ~9 month sell-off, we’re reallocating right when pessimism and exposures are at extremes.

After all, who today will admit to owning Atlassian in the United States or Xero in Australia?

This is the future of our strategy, and I think unique in the market today. It’s certainly more systematic, more risk-conscious, and more adaptive than the way we operated in the past, and we’ve now been operating it for over three years. We’ll continue to research ways to improve.

As always, markets rarely move in straight lines, and after many steps forward we’re due for a market step back. We’ve taken profits in a number of our semiconductor positions that hit their targets, but some consolidation would be normal.

We see three major risks and open questions in markets

Firstly, equity supply

There is enormous amount of capital issuance about to drain markets, and prices might move ahead of it (judging by last Friday’s sell off, they may have already started).

SpaceX is seeking to raise US$75 billion in their IPO, Alphabet is raising ~US$85 billion, including $40 billion in a program selling shares directly on market, and Meta is reportedly planning an equity raise in the tens of billions, though no transaction has been announced. Anthropic has confidentially submitted a draft S-1 for an IPO, and Open AI has raised $122 billion privately, and is also widely reported to be exploring an IPO.

This is a lot of net selling, where cash is transferred out of the otherwise zero-sum equity market pool on to these companies balance sheets.

The IPO market has been stagnant for years, so you could argue there is pent-up demand for new supply. But this is a serious $ amount for the market to digest.

This matters because indexed mutual funds and ETFs now represent a majority of US long-term fund assets. The Nasdaq-100 has also adopted a fast-entry pathway to accommodate and early entry for companies like SpaceX, which once included would require index-tracking vehicles to trim existing holdings.

Many have wondered how far the long-term trend towards passive will go. Obviously the whole market can’t be passive ETFs, but where is the limit?

This could actually be a rare opportunity for active managers to outperform. If large, obviously richly valued companies are rapidly included in indices and trend down, this would be an easy way for managers to outperform. Time will tell!

Big Picture in Big Tech

A new dynamic is emerging at the top end of town though.

The hyperscalers, the most cash-flow generative companies in history barring state oil companies and the like, are now directing cash flow to datacenter capex, and raising large amounts of debt and fresh equity to do so.

These companies used to offer a consistent buyback bid, and you could literally see markets stabilise after the inevitable chaos of each earnings season when the buyback window reopened, and the hyperscalers resumed their buybacks. Now they are doing the opposite, raising capital.

This is a new and unpredictable dynamic, but one that is almost certainly less stable.

For us, it would now be unthinkable to invest in technology, semiconductors, and growth stocks without a quant risk framework like the one we’ve developed.

The long term bull thesis is as strong as ever, with a massive global capacity expansion, but the likelihood of volatility and counter-trend bear markets looks higher than ever.

Secondly, there are threats to the business models of OpenAI and Anthropic. Will these companies maintain their positions, and what does this mean for global capex if they don’t?

Open-weight ‘free’ models (as in, the model itself is free, you still have to pay to run it) are only a few months behind state-of-the-art, and the range of tasks for which you need the highest available intelligence for is shrinking.

In our experience, Minimax M2, Kimi, Qwen, Deepseek, and in the United States Llama and new US open-weight contenders (I’m personally rooting for Arcee’s Trinity) are excellent at most of the analysis, operations and broad knowledge work we use models for.

OpenAI and Anthropic still have a significant edge in coding and more complex analysis over the free models. But this is something we are watching closely, and we’ll be delighted when we can move all these workflows to suppliers that are 90% cheaper.

Switching workflows between models is trivial. Several weeks ago we were all-in on the Claude ecosystem. We have since switched to OpenAI entirely - Codex 5.5 is just noticeably better right now.

The language model leaders are making significant efforts to lock people into their platforms, particularly in enterprise. Time will tell whether these are powerful, but for now, switching is trivial, and transferring large amounts of context between models is straightforward, and is the kind of task they are very good at anyway.

And once an open-weight model is in the public domain, it’s there forever. That’s the base level of civilizational artificial intelligence available to all. So when some new difficult task is conquered by the open-weight models, that is one less reason to pay up for Claude or ChatGPT.

Noone knows for sure how this will play out, but my guess is there will be a dust-up in the next 1-2 years and another major Deepseek moment (it may not be Deepseek the second time around).

But even if the worst case plays out for Claude and Codex, this isn’t necessarily bearish. Cheaper models will still need vastly more compute and memory than is currently available today. But if the IPO window closes, things could be nasty for US VCs who have generated the bulk of their recent returns in these companies.

For now, usage is growing so fast, and has so much further to go, that the rising tide is lifting all.

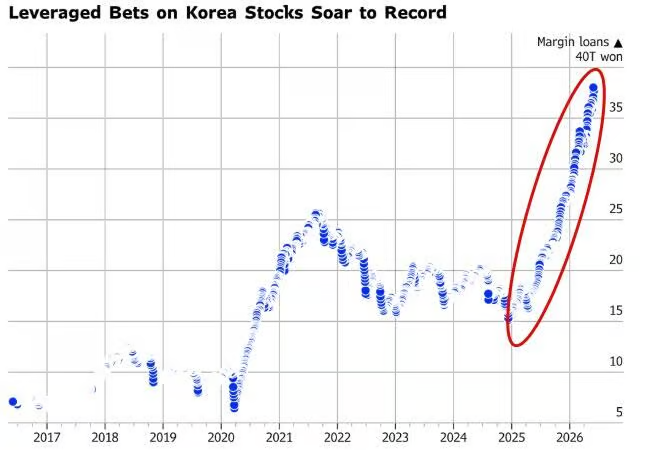

Thirdly, positioning is scarily long again, and any shock would result in serious systematic deleveraging

The same positioning indicators that suggested a fierce market rally two months ago have swung entirely to the opposite side of the spectrum, and all sorts of weird and wonderful leverage has entered the system, notably in Korean leveraged single stock and index ETFs.

Regardless of cause, a hiccup now could trigger a washout.

Closer to home, the Australian market may be challenged for some time with these new CGT rules. Every single market participant will have to adjust their models and behaviours for these new, more complicated taxes.

For a standard market washout to morph into a more serious bear market, we would likely need to see a change in direction in capex spend, which could simply be hyperscalers deciding to spend the same amount next year, as this year, ie zero growth.

We have not seen this yet, but markets have a way of sniffing these things out in advance.

Which is why our risk management processes are purely price based and so important in markets like these.

Outlook

On Friday we saw a wave of selling in tech, centered on semiconductors. There was ostensibly a catalyst, when Broadcom gave positive but slightly disappointing guidance, but this was nowhere near enough to justify such a reaction... which is useful information in its own right.

Positioning probably just reached too far.

There was an explosion in margin lending, particularly in Korea (bless), where Samsung and SK Hynix now count amongst the world’s largest companies.

Some of you have noted we haven’t discussed healthcare much lately. That is largely because the industry has been in a broad downtrend, and we either exited at profits (Day One was bought out at a healthy premium), or closed positions that disappointed like Grail and Rhythm (fortunately at a profit).

In Australia, Anteris has been a rare healthcare winner:

We always had high conviction in the technology, but like all these companies it’s a long term play, perhaps too long for most equity investors. Recent M&A activity in the US was positive, and perhaps the painful relisting in the US is finally bearing fruit.

The software sell-off was well-publicised, but there was a second bear market that was just as severe, with many so-called ‘compounders’ crushed, including those in healthcare. To give one example, look at Boston Scientific:

Or Intuitive Surgical:

These are companies we are watching for a turn, particularly if EPS growth holds up.

We are also watching fast-growing old favourites like Alnylam and argenX closely, which have also had a difficult time lately.

This is another area where our risk approach really pays off, not just on the upside in growth sectors, but also helping us avoid these kinds of sell-offs, which are highly unpredictable, but show monetizable trends (in this case, by staying out).

Finally, a reminder our ETF (ticker ASX:ROAR) listed last Monday, so if you would like information see our website, and please check in to our webinar tomorrow morning.

Good luck out there

Mike